Understanding VA Home Loans

VA home loans represent a significant financial opportunity exclusively available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. Established by the U.S. Department of Veterans Affairs, these loans are designed to provide financial backing for those who served in the military, making homeownership more accessible through various attractive features.

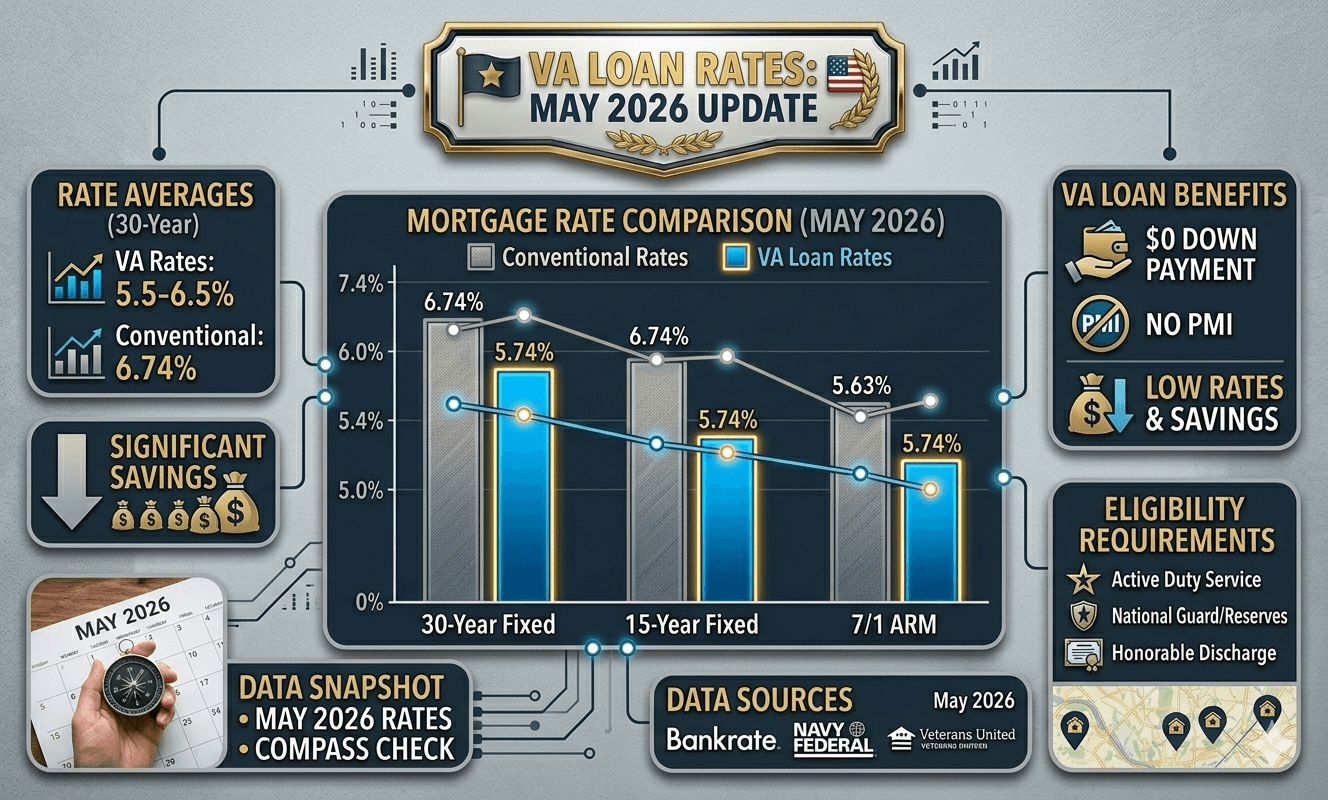

Yes, VA home loan interest rates are significantly lower than conventional mortgages right now. As of May 2026, the national average 30-year VA purchase rate is 5.50% to 6.50%, depending on which lender and data source you check . Compare that to conventional 30-year rates averaging 6.74% — a difference that saves the average veteran over $100 per month on a $300,000 loan.

🩺 Blood Pressure Monitor

Clinically validated automatic blood pressure monitor with an easy-to-read display. Great for daily home monitoring.

Check Price on Amazon →💊 Weekly Pill Organizer

Keep medications organized with a weekly pill organizer designed for easy daily use at home or while traveling.

Check Price on Amazon →🌡️ Heating Pad for Back Pain

Electric heating pad designed to help soothe back, neck and shoulder discomfort with adjustable heat settings.

Check Price on Amazon →As an Amazon Associate, we may earn from qualifying purchases.

The best VA rates available today come from military-focused lenders. Navy Federal Credit Union is offering 5.125% on 15-year VA loans and 5.375% on 30-year VA loans as of April 30, 2026 . Veterans United shows 5.500% for 30-year VA purchases with 1.563 discount points . Meanwhile, the national average 30-year VA rate is trending around 6.49% according to Bankrate’s May 12 survey .

This guide breaks down current VA rates from multiple lenders, explains why VA rates are lower than conventional loans, and shows you exactly how to lock in the best rate for your situation.

What Veterans Need to Know Right Now

The VA home loan program is one of the most powerful benefits available to veterans. The two biggest advantages? Zero down payment and interest rates that consistently undercut conventional mortgages .

🇺🇸 IMPORTANT DISCLAIMER – Veterans Benefits Information

This site provides general information about U.S. Department of Veterans Affairs (VA) benefits for educational and informational purposes only.

- Not Official: We are NOT affiliated with, endorsed by, or connected to the U.S. Department of Veterans Affairs (VA), the Veterans Benefits Administration (VBA), the Veterans Health Administration (VHA), or any other government agency.

- No Legal/Financial Advice: The content on this website is for informational purposes only and does not constitute legal, financial, or medical advice. VA benefits rules change frequently – always consult with an accredited Veterans Service Officer (VSO) or a qualified professional for your specific situation.

- Official Sources: For official, binding information and to apply for benefits, always visit official .gov websites: VA.gov, Benefits.VA.gov, or SSA.gov.

- No Data Collection: This site does not collect, store, or process any personal information. It does not have login forms, contact forms, or any system to capture user data. We never ask for your Social Security Number, bank details, or any personal information.

- 🚨 Scam Alert: The VA and other government agencies never charge fees for benefit applications. If anyone asks for money to "process" your VA claim, it is a scam. Report it to the VA Office of Inspector General at VA.gov/OIG.

- Advertising: This site uses third-party advertising (Adsterra) to cover operational costs. We do not endorse or guarantee any products or services advertised.

📌 Information provided as of June 2026. Always verify current eligibility and rules with official .gov sources.

This site is not affiliated with the U.S. Department of Veterans Affairs or any government agency. All information is for educational purposes only. Please visit VA.gov for official information.

Here is the data that matters for May 2026:

| Loan Type | VA Rate | Conventional Rate | VA Advantage |

|---|---|---|---|

| 30-Year Fixed | 5.50-6.50% | 6.74% | ~1.0% lower |

| 15-Year Fixed | 5.125-5.50% | 6.14% | ~0.8% lower |

Sources: Bankrate, Navy Federal, Veterans United

The gap between VA and conventional rates has widened slightly in early 2026. According to Experian’s March 2026 analysis, VA loans averaged 5.63% while conventional loans averaged 6.58% — nearly a full percentage point difference .

Real-life example: On a $350,000 home with zero down, a veteran with a 5.50% VA rate pays about $1,987 per month. The same home with a conventional loan at 6.58% requires a 20% down payment ($70,000) to avoid PMI, and the monthly payment is still higher at roughly $1,975. The VA buyer keeps $70,000 in their pocket AND gets a comparable payment .

Here is the catch for May 2026: Rates have been volatile. Bankrate reported the average 30-year VA APR at 6.53% on May 12, up slightly from previous weeks . If you see a rate you like, locking it in matters more than waiting for a bottom that may not come.

Latest VA Home Loan Rates Today (May 2026)

Here is the current snapshot of VA loan rates from multiple sources. All data is from May 2026.

National Average VA Rates

| Source | 30-Year VA Rate | 30-Year VA APR | Date |

|---|---|---|---|

| Bankrate | 6.49% | 6.53% | May 12, 2026 |

| Veterans United | 5.500% | 5.922% | May 2026 |

| Navy Federal | 5.375% | 5.789% | April 30, 2026 |

| Guaranteed Rate (National Avg) | 5.903% | N/A | May 8, 2026 |

| Zillow (California sample) | 6.000% | 6.249% | May 13, 2026 |

Why the Range? Understanding Rate Differences

You will notice a wide spread between “as low as” advertised rates (5.125-5.500%) and national averages (6.49-6.53%). Here is why:

Advertised rates assume perfect credit (740+), significant discount points (prepaid interest), and ideal loan conditions. National averages reflect what actual borrowers are getting across all credit profiles and point options.

What this means for you: Do not expect to walk in and automatically get 5.375% with no points. That rate requires paying discount points upfront — typically 0.5 to 1.5% of your loan amount .

15-Year VA Rates (May 2026)

| Lender | Interest Rate | APR |

|---|---|---|

| Navy Federal | 5.125% | 5.773% |

| Veterans United | 5.375% | 6.070% |

The 15-year option saves significant interest over the life of the loan but comes with higher monthly payments.

Who Qualifies for VA Home Loan Rates

VA loans are not automatic. You must meet eligibility requirements.

Eligible Borrowers

| Category | Requirement |

|---|---|

| Veterans | Honorable discharge, 90+ days active duty wartime OR 181+ days peacetime |

| Active Duty | 90+ consecutive days of service |

| National Guard/Reserve | 6+ years of service OR 90+ days active duty |

| Surviving Spouses | Of service members who died in service or from service-connected disability |

What Affects Your VA Rate

Even with VA eligibility, your specific interest rate depends on several factors:

| Factor | Impact |

|---|---|

| Credit score | 740+ gets best rates; 620-740 still qualifies but rates may be 0.25-0.5% higher |

| Debt-to-income ratio | Under 41% is ideal; higher ratios may require stronger credit |

| Discount points | Paying points upfront lowers your rate (1 point = 1% of loan amount, typically lowers rate ~0.25%) |

| Loan term | 15-year rates are lower than 30-year rates |

| Lender | Rates vary significantly between lenders — shop around |

Important: The VA does NOT set interest rates. Private lenders do. The VA guarantees the loan, which reduces lender risk, and that is why VA rates are typically lower than conventional . But rates still vary by lender.

VA Loan Rate Comparison by Lender (May 2026)

Here are specific offers from major VA lenders. Use these to benchmark your own quotes.

Navy Federal Credit Union

Rates as of April 30, 2026

| Term | Rate | Discount Points | APR |

|---|---|---|---|

| 30-Year VA | 5.375% | 0.500 | 5.789% |

| 15-Year VA | 5.125% | 0.250 | 5.773% |

Best for: Existing Navy Federal members, those with strong credit, veterans seeking the lowest advertised rates.

Veterans United Home Loans

Rates as of May 2026

| Loan Type | Rate | Discount Points | APR |

|---|---|---|---|

| 30-Year VA Purchase | 5.500% | 1.563 ($4,611 on $295k loan) | 5.922% |

| 30-Year VA Refinance | 5.625% | 2.000 ($5,900 on $295k loan) | 5.942% |

| 15-Year VA Purchase | 5.375% | 1.438 ($4,242) | 6.070% |

Best for: First-time VA buyers, veterans who want a lender that specializes exclusively in VA loans.

Bankrate National Average Survey (May 11-12, 2026)

Bankrate surveys the nation’s largest lenders. Here are representative offers :

| Lender | 30-Year VA Refi Rate | APR | Points |

|---|---|---|---|

| Mutual of Omaha Mortgage | 5.000% | 5.233% | 1.819 |

| loanDepot | 5.250% | 5.423% | 1.412 |

| Rocket Mortgage | 5.250% | 5.495% | 1.875 |

| Strong Home Mortgage | 5.250% | 5.456% | 1.625 |

Best for: Comparing multiple lender offers side by side.

Guaranteed Rate (National Average)

As of May 8, 2026, the national average 30-year VA rate reported is 5.903% .

VA Loan vs. Conventional: The Real Financial Difference

This is where the math gets compelling.

Purchase Example: $400,000 Home, 0% Down VA vs. 20% Down Conventional

| VA Loan | Conventional Loan | |

|---|---|---|

| Down payment | $0 | $80,000 (20%) |

| Interest rate | 5.50% | 6.58% |

| Monthly payment (P&I) | $2,271 | $2,042 |

| Upfront cash needed | ~$8,000 (closing costs) | ~$88,000 (down payment + closing costs) |

*Assumes VA rate from Veterans United , conventional rate from Experian March 2026 data *

The verdict: The VA buyer keeps $80,000 in savings while having a slightly higher monthly payment. Over time, that $80,000 invested elsewhere could offset the payment difference many times over.

30-Year VA vs. 15-Year VA: Which Is Better?

| Loan Type | Rate | Monthly Payment (on $300k) | Total Interest |

|---|---|---|---|

| 30-Year VA (5.50%) | 5.50% | $1,703 | $313,000 |

| 15-Year VA (5.125%) | 5.125% | $2,392 | $130,600 |

Savings with 15-year: $182,400 less in total interest. But you pay $689 more per month.

Who should choose 30-year: Veterans who want lower monthly obligations, those early in their careers, or anyone who prefers cash flow flexibility.

Who should choose 15-year: Veterans within 10-15 years of retirement, those with higher income, or anyone who wants to build equity faster and pay less total interest.

How to Get the Best VA Home Loan Rate (Step-by-Step)

Do not just accept the first rate you see. Follow these steps.

Step 1: Check your Certificate of Eligibility (COE)

You can request your COE online through the VA portal, through your lender, or by mail. Most lenders will pull it for you for free.

Step 2: Check and optimize your credit

VA loans have no official minimum credit score, but most lenders want 620-640. For the best rates, aim for 740+ .

Action items:

- Pull your free credit report from AnnualCreditReport.com

- Dispute any errors

- Pay down credit card balances to under 30% of limits

- Do not open new credit accounts before applying

Step 3: Shop at least 3-5 VA lenders

Rates vary significantly. The difference between the best and worst offer can be 0.5% or more — thousands of dollars over the life of the loan.

Lenders to check:

- Veterans United (VA specialists)

- Navy Federal (credit union, low rates)

- Rocket Mortgage (fast online process)

- loanDepot (competitive refinance rates)

- Mutual of Omaha Mortgage

Step 4: Compare APR, not just interest rate

APR includes fees and closing costs. A lower interest rate with high fees might cost you more overall. Always ask for the APR .

Step 5: Ask about discount points

Discount points are prepaid interest. One point costs 1% of your loan amount and typically lowers your rate by about 0.25%.

When to buy points: If you plan to stay in the home for 5+ years, buying points usually saves money.

When to skip points: If you might move or refinance within 3-5 years, skip the points.

Step 6: Lock your rate

Once you find a rate you like, ask for a rate lock. Locks typically last 30-60 days. Given current market volatility, locking within 24 hours of getting a quote is smart .

Step 7: Close within your lock period

If your lock expires before closing, you may have to pay a fee to extend or accept a higher rate.

Common Mistakes Veterans Make With VA Home Loan Rates

Avoid these pitfalls.

Mistake #1: Assuming the VA sets rates

Reality: The VA does NOT set interest rates. Lenders do. The VA guarantees the loan, which helps keep rates lower, but you still need to shop around .

Mistake #2: Ignoring the VA funding fee

The VA funding fee is a one-time fee of 1.25% to 3.3% of the loan amount that helps keep the VA loan program running.

| Down Payment | First-Time Use | Subsequent Use |

|---|---|---|

| 0% | 2.15% | 3.3% |

| 5% | 1.5% | 1.5% |

| 10% | 1.25% | 1.25% |

Exemption: Veterans with a service-connected disability rating (any percentage) are EXEMPT from the funding fee. Make sure your lender applies this if you qualify.

Mistake #3: Only checking one lender

Some veterans assume all VA lenders offer the same rates. They do not. Bankrate’s survey shows rates ranging from 5.00% to 6.125% from different lenders on the same day .

Fix: Get quotes from at least three lenders. Use them against each other.

Mistake #4: Not understanding discount points

A lender advertises 5.25% but does not mention it requires 2 points ($6,000 on a $300,000 loan). Another lender offers 5.75% with no points. The no-point option may be cheaper overall if you move within a few years.

Fix: Always ask: “What is your zero-point rate?” Compare that across lenders.

Mistake #5: Waiting for rates to drop further

Mortgage rates are notoriously difficult to predict. The Federal Reserve has signaled potential rate cuts later in 2026, but no one knows for sure . If you find a rate that fits your budget, lock it.

VA Loan Trends and Outlook for 2026

Here is what experts are watching.

Current Market Conditions

VA loan rates have largely fluctuated in the 6% to 7% range over the past year and a half . The current dip to the mid-5% range for some lenders represents a recent improvement.

What drives VA rates: Mortgage rates are largely influenced by the 10-year Treasury note’s yield, which moves based on investors’ expectations of future monetary policy and other economic indicators .

Current headwinds: Ongoing economic uncertainty, including questions about U.S. tariff policy and broader inflation concerns, are keeping rates higher than they might otherwise be. When investors sense market instability, they demand higher yields on bonds, which pushes mortgage rates up .

Expert Predictions

Until there is more clarity on trade policy and inflation trends, rates are unlikely to fall significantly . Some analysts expect gradual declines in late 2026 if inflation continues to cool, but near-term volatility is likely.

What this means for you: Timing the market is gambling. If you find a rate you can afford, lock it. If rates drop later, you can always refinance with a VA IRRRL (streamline refinance).

VA Refinance Rates (Current)

If you already have a VA loan and want to refinance, here is what you need to know.

Current VA Refinance Rates (May 2026)

| Source | 30-Year VA Refi Rate | APR |

|---|---|---|

| Bankrate National Avg | 6.47% | 6.51% |

| Veterans United | 5.625% | 5.942% |

| Mutual of Omaha | 5.000% | 5.233% |

Two Types of VA Refinance

IRRRL (Interest Rate Reduction Refinance Loan):

Also called a “VA Streamline Refinance.” For veterans who already have a VA loan and want a lower rate with minimal paperwork. No appraisal required. No income verification. Closing costs can be rolled into the new loan.

VA Cash-Out Refinance:

Replace your current mortgage with a larger VA loan and take the difference in cash. You can access up to 100% of your home’s equity. Rates are slightly higher than IRRRL rates.

When refinancing makes sense: If you can lower your rate by at least 0.5-0.75 percentage points and plan to stay in the home for 2+ years, refinancing usually pays off.

FAQ (What Veterans Ask Google About VA Home Loan Rates)

What are current VA home loan interest rates?

As of May 2026, 30-year VA rates range from 5.375% to 6.53% depending on the lender and your credit profile .

Are VA loan rates lower than conventional?

Yes. VA rates are typically 0.5-1.0 percentage points lower than conventional rates. Current VA average is around 5.5-6.5% vs. conventional at 6.74% .

What credit score do I need for a VA loan?

The VA has no minimum credit score, but most lenders want 620-640. For the best rates, aim for 740+ .

Does the VA set interest rates?

No. Private lenders set VA loan rates. The VA guarantees the loan but does not lend money directly .

What is the VA funding fee?

A one-time fee of 1.25% to 3.3% of the loan amount. Veterans with service-connected disabilities are exempt .

Can I get a VA loan with no down payment?

Yes. VA loans offer 0% down payment on purchases up to the conforming loan limit .

How do I find the best VA loan rate?

Shop at least 3-5 VA lenders, compare APRs not just interest rates, and ask about discount points. Check lenders like Navy Federal, Veterans United, and Rocket Mortgage .

What is a VA IRRRL?

An Interest Rate Reduction Refinance Loan that allows veterans with existing VA loans to refinance to a lower rate with minimal paperwork. No appraisal required.

Should I lock my VA loan rate now?

Given current market volatility, locking within 24 hours of getting a quote is recommended if you like the rate .

Can I use a VA loan more than once?

Yes. VA loan entitlement is reusable. If you sell your home and pay off the VA loan, you can use it again.

Final Takeaway (Actionable Summary)

VA home loan rates in May 2026 are historically favorable — especially compared to conventional options. The best rates are hovering around 5.125-5.5% for well-qualified borrowers, though national averages are closer to 6.5% .

Here is your action plan:

If you are buying a home:

- Get your COE from the VA this week

- Check your credit score and optimize if needed

- Compare rates from at least 3 VA lenders (start with Navy Federal and Veterans United)

- Ask each lender for their zero-point rate AND their rate with points

- Lock your rate as soon as you find one you like

- Close before your rate lock expires

If you are refinancing:

- Calculate your current interest rate vs. today’s VA rates

- If the difference is 0.5% or more, request quotes from 3 lenders

- Ask about IRRRL (streamline refinance) options

- Calculate your break-even point on closing costs

- Refinance if you will stay in the home past the break-even date

If you are a disabled veteran:

- Make sure your lender knows your disability rating

- Confirm you are exempt from the VA funding fee

- This saves you 2.15-3.3% of your loan amount — thousands of dollars

The bottom line: VA loans remain one of the best benefits available to American veterans. The current rates are attractive, especially compared to conventional mortgages. Do not wait for a “perfect” rate that may never come. If the numbers work for your budget, lock it in and move forward.

Your service earned you this benefit. Use it.

One of the most compelling aspects of VA home loans is their competitive interest rates, especially when compared against conventional mortgage options. In 2026, today’s VA home loan interest rates remain remarkably favorable, helping veterans and eligible borrowers save money over the life of their loans. Current statistics show that VA loans often portray rates lower than their conventional counterparts, which may typically necessitate a larger down payment and carry stricter eligibility criteria.

In the current landscape, the average VA loan interest rate has been recorded at around 2.85% to 3.25%, which presents a distinct advantage for veterans seeking to purchase a home. This reduced rate directly translates to notable long-term savings, with estimates suggesting that veterans could save thousands of dollars in interest payments when compared to traditional mortgages. Therefore, the strategic use of VA home loans can profoundly impact the financial future of those who have served in our armed forces.

In summary, understanding VA home loan interest rates and their structure is imperative for veterans aiming to navigate the home buying process effectively. By leveraging the benefits of these loans, veterans can capitalize on their unique eligibility, enjoy lower interest rates, and ultimately benefit from a smoother path to homeownership compared to conventional financing routes.

Current VA Loan Interest Rates Overview

As of May 2026, the average VA home loan interest rates reflect a competitive lending environment, favorable for eligible veterans and active service members looking to secure financing for home purchasing or refinancing. At this date, the 30-year fixed-rate VA loans are generally offered with interest rates averaging around 3.25%, while the 15-year fixed-rate options see rates that are slightly lower, typically averaging 2.85%.

Key lenders such as Navy Federal Credit Union and Veterans United continue to play a prominent role in this arena, providing various products customized to meet the diverse needs of veterans. Navy Federal currently showcases interest rates close to the average figures mentioned, with a 30-year VA loan at approximately 3.30% and a 15-year option at about 2.90%. Veterans United, on the other hand, publishes competitive rates as well, featuring a 30-year VA loan at around 3.20% and a 15-year loan at an attractive 2.85%.

This favorable rate environment for VA loans stands in contrast to conventional mortgage rates, which as of May 2026, are averaging around 4.50% for 30-year loans and roughly 3.75% for 15-year loans. The significant difference in interest rates presents a compelling argument for veterans considering a VA home loan over traditional financing options. Overall, the lower rates for VA loans, along with the absence of down payment requirements and private mortgage insurance, make these loans highly appealing for those who qualify.

Comparative Analysis of Top Lenders

When considering a VA home loan, it is essential to compare the offerings of various lenders to ensure that you secure the best interest rates and terms available. In 2026, several prominent lenders stand out in the marketplace, including military-focused lenders and traditional banks, each with unique features catered to veterans and active-duty service members.

Military-focused lenders often provide benefits tailored to the military community, such as lower interest rates and reduced fees. For instance, Lender A offers a 3.25% interest rate with zero closing costs for VA home loans, making it an attractive choice for veterans seeking minimal upfront expenses. However, while Lender A may excel in interest rates, their processing times may be longer compared to other institutions.

On the other hand, a well-known traditional bank, Lender B, presents competitive VA home loan rates of 3.5%. Despite slightly higher interest rates, they offer a streamlined online application process and quicker approval times, which might be advantageous for borrowers needing fast financing solutions. However, Lender B does include additional underwriting fees, which could impact the overall cost of the loan.

Additionally, Lender C, another military-focused institution, provides highly favorable terms, including a 3.0% interest rate but imposes a funding fee that can reach 2.3% of the loan amount. While their initial rates are appealing, borrowers must weigh the funding fee against the overall loan cost when making their decisions.

In assessing these options, it is crucial for potential borrowers to consider not only the interest rates but also the terms, conditions, and any additional fees associated with each lender’s offerings. By doing so, veterans can make informed decisions that align with their financial goals and home ownership aspirations.

Factors That Influence VA Loan Interest Rates

The interest rates associated with VA home loans are influenced by a variety of factors, each playing a significant role in determining the rates that veterans are offered. Understanding these factors is essential for veterans who wish to optimize their home financing options.

Firstly, economic conditions have a considerable impact on interest rates. When the economy is thriving, the Federal Reserve might increase interest rates to maintain equilibrium. Conversely, during economic downturns, lower interest rates may be employed to stimulate borrowing and spending. Veterans should keep an eye on the broader economic indicators, as these can directly affect the rates offered to them.

Lender policies are another critical element influencing VA loan interest rates. Different lenders may have their own criteria for assessing risk, leading to variations in loan terms and rates. Factors such as the lender’s operating costs, competitive positioning, and desire to attract veteran borrowers can result in differing rates among lenders. It is advisable for veterans to compare offers from multiple institutions to identify the most favorable rates.

Additionally, veteran eligibility can influence the loans themselves, as the VA has established guidelines that determine who can obtain a loan and at what terms. Depending on the service length and discharge status, veterans may gain access to lower rates or more flexible financing options.

Credit scores are crucial determinants of interest rates for any loan type, including VA loans. A higher credit score typically signifies lower risk to lenders, which may translate to lower interest rates. Veterans should strive to improve their credit profiles before applying for a loan.

Finally, the loan amount can also affect the VA loan interest rates. Larger loan amounts may come with different interest rate structures compared to smaller loans. Understanding these specific factors can empower veterans to make informed decisions regarding their home buying journey.

Locking in the Best VA Loan Rate

When pursuing a VA home loan, it’s essential to be proactive in securing the best possible interest rates. VA loan interest rates fluctuate frequently, influenced by broader market conditions, economic indicators, and lender practices. Therefore, understanding how to lock in favorable terms can significantly impact your overall loan affordability.

One of the most effective strategies is timing your application wisely. Monitoring market trends and economic forecasts can provide clues on when rates may rise or fall. Ideally, you should aim to apply for your VA loan when interest rates are at their lowest, often during periods of economic uncertainty or when the Federal Reserve decides to lower rates.

Once you identify an opportune time, it is crucial to secure a rate lock. A rate lock is an agreement between the borrower and the lender that guarantees a specific interest rate for a set period, which usually ranges from 30 to 60 days. This can be immensely beneficial in shielding you against sudden rate increases while your loan is being processed. Ask your lender about their rate lock options, including lock periods and any associated fees.

Additionally, ensuring your credit score is in good standing before applying can significantly influence the rates available to you. Higher credit scores typically result in lower interest rates, so managing debts and timely bill payments is vital. Another key factor is to shop around and compare lenders. Different lenders might have varying rates and terms, so obtaining multiple quotes can help you find a suitable rate lock.

In summary, locking in the best VA loan rate requires strategic timing, diligent market monitoring, and effective negotiation with lenders. By being informed and proactive, veterans can navigate the loan process more successfully, securing the best financial outcome for their home purchase.

Benefits of VA Loans Over Conventional Loans

Veterans Affairs (VA) loans offer several advantages that make them a compelling choice for eligible veterans seeking home financing. Unlike conventional loans, which often require substantial down payments, VA loans allow for a zero down payment option. This feature is especially beneficial for veterans transitioning into homeownership, as it alleviates the immediate financial burden typically associated with purchasing a home. By enabling veterans to finance their homes with little to no upfront cost, VA loans play a crucial role in making homeownership more accessible.

Additionally, VA loans do not require private mortgage insurance (PMI), which is usually mandated for traditional loans when the down payment is less than 20%. The absence of PMI can result in significant savings over the life of the loan. This further enhances affordability, allowing veterans to allocate their financial resources towards other necessities or savings, rather than insurance premiums. As such, this characteristic of VA loans distinctly positions them as a favorable option for veterans in the housing market.

Another notable advantage of VA loans is their competitive interest rates. VA lenders typically offer lower rates compared to conventional loans, contributing to reduced monthly payments. This not only increases the purchasing power of veterans but also can lead to significant savings throughout the entire loan term. As eligibility is based on service, veterans can take advantage of these favorable terms, which reflect the government’s recognition of their service. Overall, the combination of no down payment, the absence of PMI, and competitive interest rates makes VA loans a particularly valuable option for eligible veterans seeking to invest in a home.

Challenges and Considerations in Securing a VA Loan

Securing a VA home loan can be a viable option for veterans, but there are several challenges and considerations to be aware of throughout the application process. One significant hurdle is the stringent lender requirements, which can vary between institutions. While the Department of Veterans Affairs (VA) guarantees a portion of each loan, lenders ultimately decide whether to approve or deny applications based on their individual criteria, which may include credit scores, income verification, and overall financial stability.

Another challenge many veterans encounter relates to the complexity of paperwork. The VA loan application process requires various forms, including proof of military service, income documentation, and any relevant financial records. Organizing these documents can be daunting for applicants, especially if they are unfamiliar with the documentation needed. To help alleviate this concern, it is advisable for veterans to compile their necessary documents in advance and maintain organized folders for quick access during their application process.

Furthermore, veterans must be cautious about potential real estate market fluctuations that may affect their loan approval and home buying process. Properties must meet specific VA appraisal standards, and if the market shifts, the home may be valued differently than anticipated. Ensuring that the selected property is compliant with VA requirements before engaging with the lender can save time and effort.

To navigate these challenges effectively, it is beneficial for veterans to seek guidance from approved VA lenders who specialize in VA loans. These professionals can provide insights about common pitfalls and help streamline the application process. Additionally, utilizing resources such as local veteran service organizations can offer valuable information and support. By preparing for these potential obstacles before beginning the loan application process, veterans can improve their chances of a successful loan approval.

Frequently Asked Questions (FAQs) about VA Loan Interest Rates

Many veterans and active-duty service members have questions regarding VA loan interest rates. Understanding these rates is crucial for making informed financial decisions when considering a VA loan for a home purchase or refinance. This section aims to address the most common inquiries.

What are the eligibility requirements for VA loans? VA loans are available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. Eligibility is generally determined based on service length, discharge type, and other factors as noted in the Certificate of Eligibility (COE). It is recommended that applicants check their eligibility early in the application process to streamline the approval.

How can I compare VA loan interest rates from different lenders? Comparing VA loan interest rates involves evaluating offers from multiple lenders. Prospective borrowers should obtain Loan Estimates (LEs) from different institutions outlining the terms of the loan, including interest rates, fees, and other costs. Online tools and calculators can assist in this process, allowing veterans to gauge how different rates impact monthly payments and overall borrowing costs.

Why do VA loan interest rates fluctuate? Interest rates on VA loans can fluctuate due to various factors, including economic conditions, inflation, and national monetary policies. These rates are also influenced by the lender’s assessment of risk and the overall demand for VA loans in the market. It’s important for borrowers to stay informed and monitor these changes, as a slight variation in interest rates can significantly impact long-term financial obligations.

Veterans considering a VA loan should explore these aspects carefully to better understand the terms associated with their potential loan, allowing for optimal financial planning and decision-making.

Conclusion and Call to Action

As we have explored throughout this blog post, understanding the intricacies of VA home loan interest rates in 2026 is crucial for veterans seeking to make informed decisions regarding their home financing options. The landscape of VA loans offers not only competitive interest rates but also various incentives that can significantly lower the overall cost of homeownership. It is important for veterans and active-duty service members to consider their unique financial situations and how these rates apply to them.

In assessing the best rates and comparing different lenders, veterans can save thousands over the life of their loan. Each lender may present varying interest rates and terms, making it vital to conduct thorough research and utilize available resources to guide your decision-making process. Furthermore, the VA loan program, with its benefits such as no down payment and no private mortgage insurance (PMI) requirements, can be tailored to fit the veteran’s financial profile, further enhancing affordability.

In conclusion, navigating VA home loan interest rates and making informed comparisons among lenders is an important step for veterans aiming to achieve their homeownership goals. We encourage you to actively explore your VA loan options and consider how different interest rates may impact your long-term financial health. Take the time to evaluate lenders, request quotes, and understand which options are best suited for your circumstances. By doing so, you can maximize the benefits provided by the VA loan program and enjoy the security of owning your own home.