Understanding VA Loans and Interest Rates

VA loans are mortgage loans that are backed by the U.S. Department of Veterans Affairs, designed specifically for veterans, active-duty service members, and certain members of the National Guard and Reserves. These loans provide a valuable opportunity for eligible individuals to purchase homes with favorable terms, reducing the barriers associated with traditional financing options.

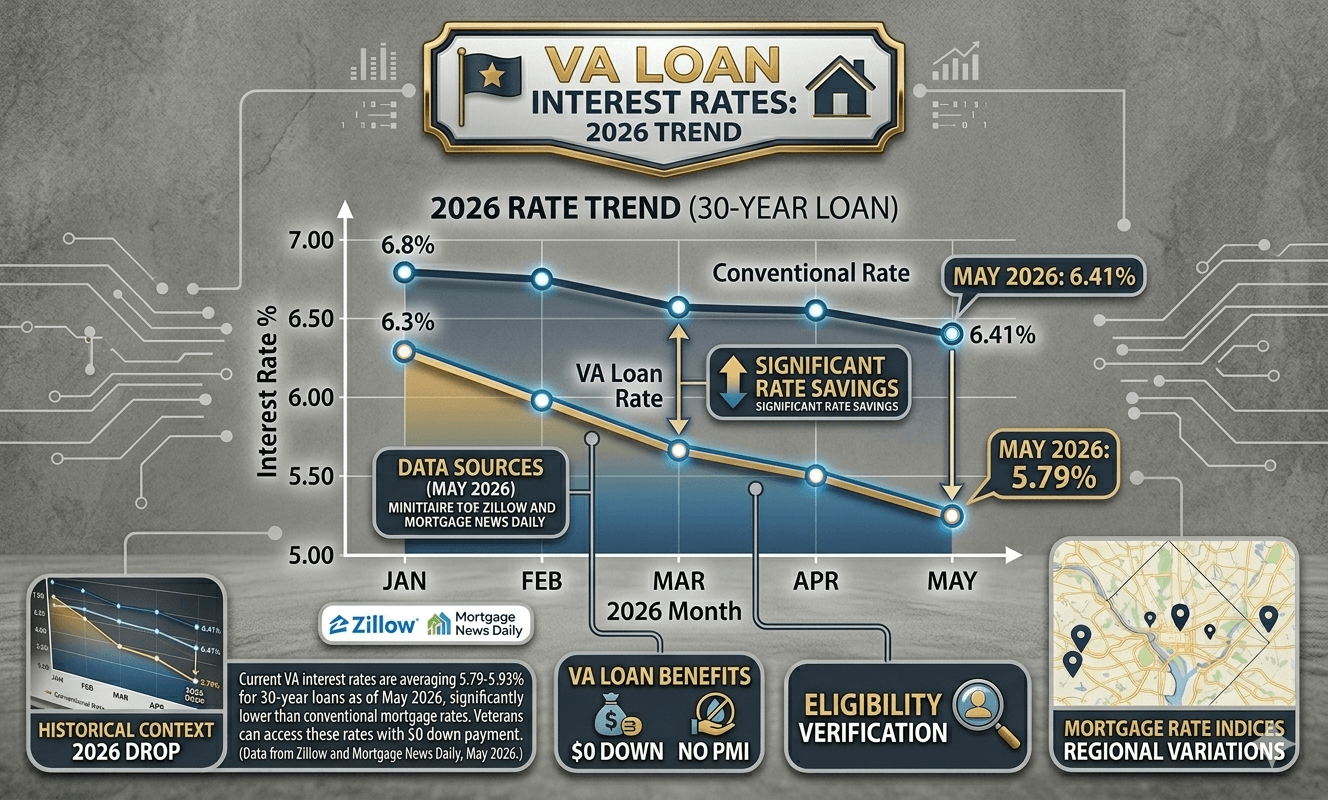

Yes, as of today (May 16, 2026), the average 30-year VA loan interest rate is 5.79% to 5.93%, depending on which lender and data source you check . This is nearly a full percentage point lower than conventional 30-year mortgage rates, which are currently hovering around 6.41% .

🩺 Blood Pressure Monitor

Clinically validated automatic blood pressure monitor with an easy-to-read display. Great for daily home monitoring.

Check Price on Amazon →💊 Weekly Pill Organizer

Keep medications organized with a weekly pill organizer designed for easy daily use at home or while traveling.

Check Price on Amazon →🌡️ Heating Pad for Back Pain

Electric heating pad designed to help soothe back, neck and shoulder discomfort with adjustable heat settings.

Check Price on Amazon →As an Amazon Associate, we may earn from qualifying purchases.

The best rates today come from military-focused lenders like Navy Federal Credit Union, which is offering a 5.25% rate (5.685% APR) on 30-year VA loans as a special Military Appreciation Month promotion through the end of May . That is a full 0.25% below their usual rates. If you are a veteran or active-duty service member, this is the best time in months to lock in a VA loan.

This guide breaks down current VA rates, how they compare to other loan types, and exactly how to get the lowest rate available to you.

What Veterans Need to Know Right Now

The VA loan program remains one of the best benefits available to U.S. veterans. The biggest advantage? No down payment required. That alone saves the average veteran tens of thousands of dollars compared to conventional loans.

🇺🇸 IMPORTANT DISCLAIMER – Veterans Benefits Information

This site provides general information about U.S. Department of Veterans Affairs (VA) benefits for educational and informational purposes only.

- Not Official: We are NOT affiliated with, endorsed by, or connected to the U.S. Department of Veterans Affairs (VA), the Veterans Benefits Administration (VBA), the Veterans Health Administration (VHA), or any other government agency.

- No Legal/Financial Advice: The content on this website is for informational purposes only and does not constitute legal, financial, or medical advice. VA benefits rules change frequently – always consult with an accredited Veterans Service Officer (VSO) or a qualified professional for your specific situation.

- Official Sources: For official, binding information and to apply for benefits, always visit official .gov websites: VA.gov, Benefits.VA.gov, or SSA.gov.

- No Data Collection: This site does not collect, store, or process any personal information. It does not have login forms, contact forms, or any system to capture user data. We never ask for your Social Security Number, bank details, or any personal information.

- 🚨 Scam Alert: The VA and other government agencies never charge fees for benefit applications. If anyone asks for money to "process" your VA claim, it is a scam. Report it to the VA Office of Inspector General at VA.gov/OIG.

- Advertising: This site uses third-party advertising (Adsterra) to cover operational costs. We do not endorse or guarantee any products or services advertised.

📌 Information provided as of June 2026. Always verify current eligibility and rules with official .gov sources.

This site is not affiliated with the U.S. Department of Veterans Affairs or any government agency. All information is for educational purposes only. Please visit VA.gov for official information.

But here is what many veterans don’t realize: VA loan rates are consistently lower than conventional rates. Right now, the gap is about 0.6 percentage points (5.8% VA vs. 6.4% conventional) . On a $300,000 loan, that difference saves you roughly $110 per month and nearly $40,000 in interest over 30 years.

Here is the catch for May 2026: Rates have been volatile. They jumped 14 basis points on May 15th alone due to rising Treasury yields . If you see a rate you like, locking it in matters more than waiting for a “perfect” bottom that may not come.

Real-life example: An Army veteran in Texas checked VA rates on May 14th and saw 5.79%. By May 16th, some lenders had already adjusted upward . He locked his rate on May 15th and saved himself a potential 0.2% increase.

Latest VA Interest Rates Today (May 2026)

Here is the current snapshot of VA loan rates from multiple sources. All data is from May 14-16, 2026.

National Average VA Loan Rates

| Loan Type | Interest Rate (5/16) | Interest Rate (5/15) | Trend |

|---|---|---|---|

| 30-Year VA | 5.83% | 5.79% | ⬆️ Up |

| 15-Year VA | 5.49% | 5.51% | ➡️ Stable |

| 5/1 VA ARM | 5.47% | 5.41% | ⬆️ Up |

Best VA Rates from Major Lenders

| Lender | 30-Year VA Rate | 30-Year VA APR | Notes |

|---|---|---|---|

| Navy Federal Credit Union | 5.25% | 5.685% | Military Appreciation Month discount (ends May 31) |

| Total Mortgage | 5.875% | 6.465% | As low as, updated May 4 |

| Zillow Marketplace Average | 5.83% | N/A | National lender average |

| Mortgage News Daily Index | 5.93% | N/A | Daily MND survey |

Rate Comparison: VA vs. Other Loan Types (May 16, 2026)

| Loan Type | Interest Rate |

|---|---|

| 30-Year VA | 5.83% |

| 30-Year Conventional | 6.41% |

| 30-Year FHA | 6.35% |

| 15-Year VA | 5.49% |

| 15-Year Conventional | 5.80% |

Source: Yahoo Finance / Zillow data

The VA advantage is clear. In every category, VA rates are lower than conventional and FHA alternatives.

Who Qualifies for VA Loan Rates

VA loans are not automatic. You must meet eligibility requirements.

Eligible Borrowers

- Veterans with an honorable discharge after 90+ days of active duty during wartime OR 181+ days during peacetime

- Active-duty service members with 90+ consecutive days of service

- National Guard and Reserve members with 6+ years of service (or 90+ days active duty)

- Surviving spouses of service members who died in service or from a service-connected disability

What You Need to Apply

- Certificate of Eligibility (COE) from the VA

- DD214 (for veterans) or current military ID (for active duty)

- Proof of income and employment

- Acceptable credit score (most lenders want 620+)

Important: There is no minimum credit score set by the VA. But individual lenders set their own requirements. Most want at least 580-620.

The “No Down Payment” Rule

Unlike conventional loans that typically require 3-20% down, VA loans allow 0% down on purchases up to the conforming loan limit (currently $806,500 in most areas) . This is the single biggest financial benefit of the program.

How to Get the Best VA Interest Rate (Step-by-Step)

Do not just accept the first rate you see. Follow these steps.

Step 1: Check your VA home loan eligibility

Get your Certificate of Eligibility (COE) from the VA. You can request it online through the VA portal, by mail using VA Form 26-1880, or through your lender (most will pull it for you for free).

Step 2: Shop at least 3-5 VA lenders

Not all VA lenders offer the same rates. Credit unions like Navy Federal often beat national banks. Online lenders may offer competitive rates but slower service. Mortgage brokers can shop multiple lenders at once.

Step 3: Compare APR, not just interest rate

The APR includes fees and closing costs. A lower interest rate with high fees might cost you more overall. Always ask for the APR .

Step 4: Ask about discount points

Discount points are prepaid interest. One point costs 1% of your loan amount and typically lowers your rate by 0.25%. If you plan to stay in the home for 5+ years, buying points can save money. If you are moving soon, skip them.

Step 5: Lock your rate

Once you find a rate you like, ask for a rate lock. Locks typically last 30-60 days. Some lenders charge a fee; many do not. Given current volatility, locking within 24 hours of getting a quote is smart.

Step 6: Close within the lock period

If your lock expires before closing, you may have to pay a fee to extend or accept a higher rate. Plan your timeline carefully.

Special Alert: Military Appreciation Month Promotion (May 2026)

Here is a time-sensitive opportunity for veterans reading this in May 2026.

Navy Federal Credit Union has lowered its VA loan rates by 0.25% for the entire month of May as part of Military Appreciation Month .

Current Navy Federal VA rates (May 12-31, 2026):

- 30-year VA: 5.250% (5.685% APR)

- 15-year VA: 4.875% (5.558% APR)

These rates are significantly below the national average. But they come with discount points:

- 30-year: 0.750 points

- 15-year: 0.500 points

What discount points mean for you: On a $300,000 loan, 0.750 points costs $2,250 upfront. Your interest rate drops by roughly 0.25% compared to their no-points rate. You break even on that $2,250 in about 3-4 years of lower monthly payments.

Important: This promotion ends May 31, 2026 . If you are considering a VA loan, this month is the time to act.

Common Mistakes Veterans Make With VA Loan Rates

These mistakes cost veterans real money.

Mistake #1: Assuming the VA sets interest rates

Reality: The VA does NOT set interest rates. The VA guarantees the loan, but private lenders set the rates. That means rates vary widely between lenders. Shop around.

Mistake #2: Ignoring the VA funding fee

Reality: Most VA loans include a funding fee (1.25% to 3.3% of the loan amount) that helps keep the program running. Veterans with service-connected disabilities are exempt. First-time users with 0% down pay 2.15%. This fee can be rolled into the loan, but it increases your total cost.

Mistake #3: Not checking your VA disability status

Reality: If you have a VA disability rating (even 10%), you are exempt from the VA funding fee. This saves you thousands. Make sure your lender applies this exemption.

Mistake #4: Focusing only on the rate, not the terms

Reality: A 5.25% rate sounds great, but if it comes with 2 points ($6,000 on a $300,000 loan) and high closing costs, a 5.5% rate with no points might be cheaper overall. Always compare APRs.

Mistake #5: Waiting for rates to drop further

Reality: Mortgage rates are notoriously difficult to predict. The Federal Reserve has signaled potential rate cuts later in 2026, but no one knows for sure. If you find a rate that fits your budget, lock it.

VA Refinance Rates (Current)

If you already have a VA loan and want to refinance, here is what you need to know.

Current VA Refinance Rates (May 16, 2026)

| Loan Type | Refinance Rate |

|---|---|

| 30-Year VA Refi | 5.83% |

| 15-Year VA Refi | 5.53% |

Refinance rates are often slightly higher than purchase rates, but the gap is minimal right now .

Two Types of VA Refinance

Interest Rate Reduction Refinance Loan (IRRRL):

Also called a “VA Streamline Refinance.” This is for veterans who already have a VA loan and want a lower rate with minimal paperwork. No appraisal required. No income verification. Closing costs can be rolled into the new loan.

VA Cash-Out Refinance:

Replace your current mortgage with a larger VA loan and take the difference in cash. You can access up to 100% of your home’s equity . Rates are slightly higher than IRRRL rates.

When refinancing makes sense: If you can lower your rate by at least 0.5-0.75 percentage points and plan to stay in the home for 2+ years, refinancing usually pays off.

What This Means Financially (Real Dollar Examples)

Let us put these rate differences into real numbers.

Purchase Example: $350,000 Home, 0% Down VA Loan

| Rate Scenario | Interest Rate | Monthly Payment (P&I) | 30-Year Total Interest |

|---|---|---|---|

| Best VA Rate (Navy Federal) | 5.25% | $1,932 | $345,520 |

| Average VA Rate | 5.83% | $2,057 | $390,520 |

| Conventional Rate | 6.41% | $2,190 | $438,400 |

Savings from best VA rate vs. average VA rate: $125/month, $45,000 over 30 years

Savings from VA vs. conventional: $258/month, $92,880 over 30 years

Refinance Example: $250,000 Remaining Balance

| Current Rate | New VA Rate | Monthly Savings | Break-Even (with $3,000 closing costs) |

|---|---|---|---|

| 6.50% | 5.50% | $160 | 19 months |

| 6.00% | 5.25% | $115 | 26 months |

| 5.75% | 5.25% | $75 | 40 months |

If you plan to stay in the home longer than the break-even period, refinancing makes financial sense.

Political and Economic Context (Why Rates Are Where They Are)

Understanding why rates move helps you make better decisions.

The Federal Reserve effect: The Fed has signaled potential rate cuts later in 2026, but inflation remains stubborn. Mortgage rates are not directly tied to the Fed funds rate, but they follow the 10-year Treasury yield. When Treasury yields rise, mortgage rates rise .

Current economic indicators (May 2026):

- 10-year Treasury yield: Trending upward

- Inflation: Above the Fed’s 2% target

- Jobs market: Still strong

Expert predictions: Analysts expect mortgage rates to gradually decline in late 2026 IF inflation continues to cool. But near-term volatility is likely .

What this means for you: Timing the market is gambling. If you find a rate you can afford, lock it. If rates drop later, you can always refinance.

FAQ (What Veterans Ask Google About VA Interest Rates)

What is the current VA interest rate?

As of May 16, 2026, the average 30-year VA rate is 5.79% to 5.93%, depending on the lender . Navy Federal offers 5.25% through May 31 .

Are VA loan rates lower than conventional?

Yes. VA rates are typically 0.5-1.0 percentage points lower than conventional rates. Current VA average is 5.83% vs. conventional 6.41% .

Does the VA set interest rates?

No. Private lenders set VA loan rates. The VA guarantees the loan but does not lend money directly .

What is the VA funding fee?

A one-time fee of 1.25% to 3.3% of the loan amount that helps fund the VA loan program. Veterans with service-connected disabilities are exempt.

Can I get a VA loan with bad credit?

The VA does not have a minimum credit score. Most lenders want 580-620. Some will go lower with compensating factors (higher income, more savings).

What is a VA IRRRL?

An Interest Rate Reduction Refinance Loan (IRRRL) allows veterans with existing VA loans to refinance to a lower rate with minimal paperwork. No appraisal required .

How often do VA rates change?

Daily. Sometimes multiple times per day. Rates are tied to bond markets, which react to economic news in real time .

Should I lock my VA loan rate now?

Given recent volatility (rates jumped 14 basis points on May 15 ), locking within 24 hours of getting a quote is recommended if you like the rate.

What is the difference between interest rate and APR?

Interest rate is the cost of borrowing money. APR includes interest plus fees and closing costs. APR is a better comparison tool between lenders .

Can I use a VA loan more than once?

Yes. VA loan entitlement is reusable. If you sell your home and pay off the VA loan, you can use it again.

Final Takeaway (Actionable Summary)

VA loans remain one of the best benefits available to American veterans. The current interest rates—averaging around 5.8% for a 30-year loan—are significantly lower than conventional rates and represent a real opportunity to save money.

Here is your action plan for May 2026:

If you are buying a home:

- Get your COE from the VA this week

- Check Navy Federal’s 5.25% promotion (ends May 31)

- Compare rates from at least 3 VA lenders

- Lock your rate as soon as you find one you like

- Close before your rate lock expires

If you are refinancing:

- Calculate your current interest rate vs. today’s VA rates

- If the difference is 0.5% or more, request quotes from 3 lenders

- Ask about IRRRL (streamline refinance) options

- Calculate your break-even point on closing costs

- Refinance if you will stay in the home past the break-even date

If you are a disabled veteran:

- Make sure your lender knows your disability rating

- Confirm you are exempt from the VA funding fee

- This saves you 2.15-3.3% of your loan amount

The bottom line: VA rates are attractive right now, especially with the Military Appreciation Month promotion. Do not wait for a “perfect” rate that may never come. If the numbers work for your budget, lock it in and move forward.

Your service earned you this benefit. Use it.

One key difference between VA loans and conventional loans lies in the requirement for private mortgage insurance (PMI). While conventional loans often require PMI if the down payment is below 20%, VA loans do not necessitate this additional cost, which can significantly lower the monthly payment for borrowers. This feature, combined with competitive interest rates, makes VA loans an attractive option for home buyers.

The interest rates on VA loans are critical indicators for potential borrowers. VA loan rates can be lower compared to rates for conventional loans, reflecting the government’s support and the overall risk profile of borrowers. The lower interest rates serve to reduce the total cost of borrowing, resulting in substantial savings over the life of the mortgage. For veterans and service members, this translates into a powerful financial advantage, allowing them to invest more in their future.

Moreover, the significance of VA loans extends beyond mere financial terms. They are a recognition of the sacrifices made by service members in defense of the country. By offering such loan programs, the VA aims to ensure that these individuals have access to affordable housing, thereby supporting their reintegration into civilian life. Understanding how interest rates interact with VA loans is essential for borrowers to make informed decisions and secure the best possible financing for their home buying journey.

Current VA Interest Rates as of May 2026

As of May 2026, the current VA interest rates for 30-year loans range from 5.79% to 5.93%. These rates reflect various factors influencing the current lending landscape, including economic conditions and lender-specific policies. The VA home loan program, designed to benefit eligible veterans and active military personnel, continues to provide opportunities for affordable home financing through competitive interest rates.

Several elements can impact these current VA interest rates. First, the overall economic environment plays a significant role. Factors such as inflation, employment rates, and consumer spending patterns can create fluctuations in interest rates. For instance, if inflation rises, lenders may increase interest rates to maintain their profit margins and protect against potential losses. Conversely, a stable economic situation may prompt lenders to offer lower rates to attract borrowers.

Additionally, the Federal Reserve’s monetary policy decisions significantly influence VA interest rates. Changes in the federal funds rate can shift market dynamics, affecting how lenders price their loan products, including VA loans. When the Fed opts to lower rates to stimulate the economy, VA loan rates often follow suit. On the other hand, an increase in the federal funds rate can lead to higher VA interest rates in the short term.

Lender policies also play a critical role in setting interest rates. Each lender may have unique criteria for determining their rates based on their business model, risk assessment, and cost of capital. Borrowers are encouraged to shop around to compare current VA interest rates across lenders to ensure they secure the most favorable terms available.

Comparison of VA Loans vs Conventional Loans

When considering financing options for home purchases, both VA loans and conventional loans merit careful consideration. One of the primary distinctions lies in interest rates. Typically, VA loans offer lower interest rates compared to conventional loans, translating to substantial savings over time. These competitive rates stem from the backing provided by the U.S. Department of Veterans Affairs, which reduces the lender’s risk.

Another significant difference is during the down payment phase. VA loans are particularly advantageous for eligible veterans and active service members, allowing them to purchase a home with zero down payment. In contrast, conventional loans usually require a down payment ranging from 3% to 20% of the home’s purchase price. This feature not only makes homeownership more accessible but also alleviates financial strain for veterans who may prefer to allocate funds elsewhere, such as for education or planning for future expenses.

Mortgage insurance requirements further differentiate these two loan types. VA loans do not require private mortgage insurance (PMI), which is necessary for many conventional loans when the down payment is less than 20%. This absence of PMI can lead to lower monthly payments, enhancing the affordability of home financing for veterans. On the other hand, borrowers with conventional loans often face the burden of ongoing insurance costs, which can significantly impact overall financial planning.

In addition to cost benefits, VA loans come with further perks, such as flexible credit requirements and no prepayment penalties. These advantages make VA loans a compelling option for qualified individuals, effectively supporting their journey toward homeownership without unnecessary financial pressures. Therefore, for veterans, utilizing a VA loan is not only a practical choice but could also be fiscally prudent, allowing them to maximize their investment in real estate.

Lender Comparisons for VA Loans

When exploring VA loans, understanding the landscape of available lenders is crucial for borrowers to make informed decisions. Several financial institutions currently offer competitive rates and favorable terms that may cater to different financial needs and preferences.

Navy Federal Credit Union is a notable player in the market, primarily serving members of the military and their families. With recent VA interest rates hovering around 4.25%, Navy Federal stands out not only for its competitive rates but also for its streamlined application process tailored for veterans. Their offerings often include zero down payment options, making homeownership accessible for those who might find traditional funding challenging.

Another lender worthy of consideration is Veterans United Home Loans, which specializes exclusively in VA financing. Their current interest rates are similarly competitive, with many borrowers reporting rates of approximately 4.375%. Veterans United also provides robust educational resources for first-time homebuyers and veterans, enhancing their appeal through comprehensive customer service and support.

Caliber Home Loans is another lender that has made inroads in the VA loan market, offering flexible terms with interest rates around 4.5%. Their advantage lies in a wide variety of loan products and customization options that can cater to the unique financial situations of veterans. They also feature user-friendly online tools, which can simplify the borrowing process for potential homeowners.

In contrast, USAA offers specialized financial services aimed at military members, with current VA loan rates reported at approximately 4.3%. Their commitment to service, along with an array of additional benefits like insurance products and financial advice tailored for active-duty members and veterans, establishes them as a formidable option within the VA loan landscape.

Each of these lenders presents unique advantages that can affect a borrower’s choice. It is advisable for veterans and active-duty service members to evaluate each option based on individual financial circumstances to secure the best deal possible in today’s competitive VA loan market.

Military Appreciation Month Discounts

Military Appreciation Month, celebrated every May, provides a unique opportunity for veterans, active-duty service members, and their families to take advantage of exclusive discounts and offers. Many financial institutions and retailers recognize the sacrifices made by military personnel and therefore extend special promotions during this month. One notable example is the Navy Federal Credit Union, which often introduces attractive rates and incentives for VA loan products and other financial services.

During Military Appreciation Month, veterans may benefit from reduced interest rates on loans, waived fees for application processes, and enhanced benefits on products such as home insurance and other financial offerings. The Navy Federal Credit Union has, in previous years, offered specific loan discounts that could be particularly advantageous for veterans looking to secure a VA loan. These offers not only alleviate some financial burdens but also signify a well-deserved recognition of service.

Furthermore, participating retailers, fuel stations, and restaurants frequently provide special discounts or cashback rewards for military members, allowing them to save on everyday expenses. This approach not only helps in alleviating the cost of living but also fosters a sense of community and appreciation that is essential for veterans and their families.

As veterans review their financial options during Military Appreciation Month, it is prudent to explore such discounts thoroughly. Each financial institution may vary in the specific terms and conditions of offers, but the potential savings from reduced interest rates and lower fees can significantly improve overall financial health. Emphasizing the importance of this month can enhance the support network available to service members, making it a valuable time to consider financial and housing options for the future.

Expert Predictions for VA Interest Rates

As we look towards the future of VA interest rates in 2026, insights from financial experts suggest several key considerations that may influence the trajectory of these rates. Experts believe that various economic factors, including inflation trends, employment rates, and overall economic recovery, will play a substantial role in shaping VA loan rates moving forward. Currently, VA loan rates are seen as competitive, but changes in the economic landscape could lead to adjustments.

One major factor that analysts are keeping an eye on is the Federal Reserve’s monetary policy. Recent indications suggest that interest rates may be held steady or increased in response to inflationary pressures. Should this occur, borrowers seeking VA loans might experience higher interest rates as lenders adjust their offerings to align with the broader financial environment. Experts recommend that potential borrowers stay informed about Fed announcements and market reactions to these decisions.

Additionally, the housing market’s performance is a critical consideration. As demand for housing continues to fluctuate due to economic conditions, the supply-demand dynamic can directly impact VA interest rates. Experts predict that if housing demand remains strong, lenders may tighten their lending criteria, potentially leading to higher rates for VA loans. Conversely, if the market softens, there could be opportunities for more favorable terms for VA borrowers.

Lastly, experts emphasize the importance of monitoring geopolitical factors and their impact on the economy. Global events can create uncertainties that lead to volatility in the financial markets, affecting interest rates across the board. As such, it is advisable for VA loan seekers to remain proactive and consider all potential market influences when planning their financing strategies.

How to Secure the Lowest VA Loan Rate

Securing the lowest possible VA loan rates is crucial for veterans and service members looking to optimize their financial investment in a home. The first step towards achieving favorable rates is to improve your credit score. Lenders often consider credit scores as a primary factor in determining loan eligibility and interest rates. A higher score not only enhances your chances of getting approved but may also lead to lower rates. Strategies for credit score improvement include paying bills on time, reducing outstanding debts, and checking your credit report for errors that can be rectified.

Another significant strategy to secure competitive VA loan rates entails shopping around for lenders. It is vital to compare offers from multiple lenders as rates can vary significantly. Each lender has unique criteria which can lead to differences in their assessments of your financial situation. Inquire about any fees or closing costs associated with the loan, as these can impact the overall cost of financing. Additionally, getting pre-approved by several lenders provides you with leverage when negotiating terms and rates.

The timing of your application can also play a role in securing a low interest rate. Keeping an eye on market trends and interest rate fluctuations is essential; applying during periods of lower rates can save you substantial money over the life of your loan. Consider locking in your rate if you find a favorable one, as this can protect you from potential increases before closing. By effectively managing your credit, comparing lenders, and timing your application wisely, you can significantly enhance your chances of obtaining the best VA loan rates available.

Qualifying for a VA Loan

Obtaining a VA loan offers numerous advantages to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. These loans, guaranteed by the U.S. Department of Veterans Affairs, provide competitive interest rates and favorable terms without the requirement for a down payment. However, to qualify for a VA loan, applicants must meet specific eligibility criteria.

One of the primary factors considered for qualification is the length of service. Borrowers typically need to have completed a minimum duration of active duty, which generally spans 90 days during wartime or 181 days during peacetime. Additionally, for those in the National Guard and Reserves, a minimum of six years of service is typically mandated unless called to active duty.

Discharge status is another essential aspect of eligibility. Applicants must have received an honorable discharge to be considered for a VA loan. Conditions such as medical discharge or release due to a service-connected disability do not disqualify applicants, provided the proper documentation is presented. Government guidelines emphasize the importance of this criterion to ensure that the benefits of a VA loan are directed towards those who have honorably served their country.

Furthermore, individuals seeking a VA loan must present relevant documentation to demonstrate their eligibility. This documentation usually includes a Certificate of Eligibility (COE), which details the applicant’s service history. Obtaining a COE can be done through the VA’s website or via direct application to the local VA office. This certificate is vital as it outlines the terms of the VA loan guarantee which significantly eases the loan approval process.

In summary, meeting the eligibility requirements for a VA loan involves demonstrating the appropriate service length, ensuring an honorable discharge, and providing necessary documentation such as the Certificate of Eligibility. By adhering to these guidelines, qualified applicants can successfully navigate the process of securing a VA loan and benefit from its unique offerings.

Conclusion and Next Steps

In reviewing the current VA interest rates as of May 2026, it is evident that there are favorable conditions for veterans and active military personnel looking to secure home financing. The rates available today are competitive, reflecting a market that encourages homeownership among those who have served our country. Given the constantly evolving landscape of interest rates, acting swiftly can be advantageous. It is crucial to compare different lenders to find the best possible rates and terms suited to your financial situation.

Throughout this post, we have examined not only the current VA loan rates but also their implications on affordability and financial planning. The potential savings from lower interest rates can translate into significant long-term benefits for borrowers. As such, it is advisable for veterans to utilize this favorable interest rate environment by seeking loans that align with their personal financial goals.

For those interested in exploring their options further, it is recommended to reach out to multiple lenders for personalized quotes. Many lenders offer online tools and calculators, which can help in estimating payments and understanding the overall cost of the loan. Additionally, gathering information on different types of VA loans can enhance your decision-making process. The more knowledge you acquire about rates and lender offerings, the better equipped you will be to make an informed choice.

In conclusion, as we see a promising trend in VA loan rates, taking proactive steps is essential. Speak with financial advisors, compare lenders, and do not hesitate to ask questions when seeking assistance. With the right approach, you can leverage the current market situation to your advantage and achieve your homeownership aspirations.