Introduction to VA Loans

VA loans are a unique type of mortgage specifically designed to assist veterans, active duty service members, and certain members of the National Guard and Reserves in purchasing homes. These loans are backed by the U.S. Department of Veterans Affairs (VA), which significantly reduces the financial burden associated with obtaining a mortgage. One of the most remarkable benefits of VA loans is the possibility of obtaining a home without a down payment, making it easier for military personnel to secure housing without the typical cost barriers.

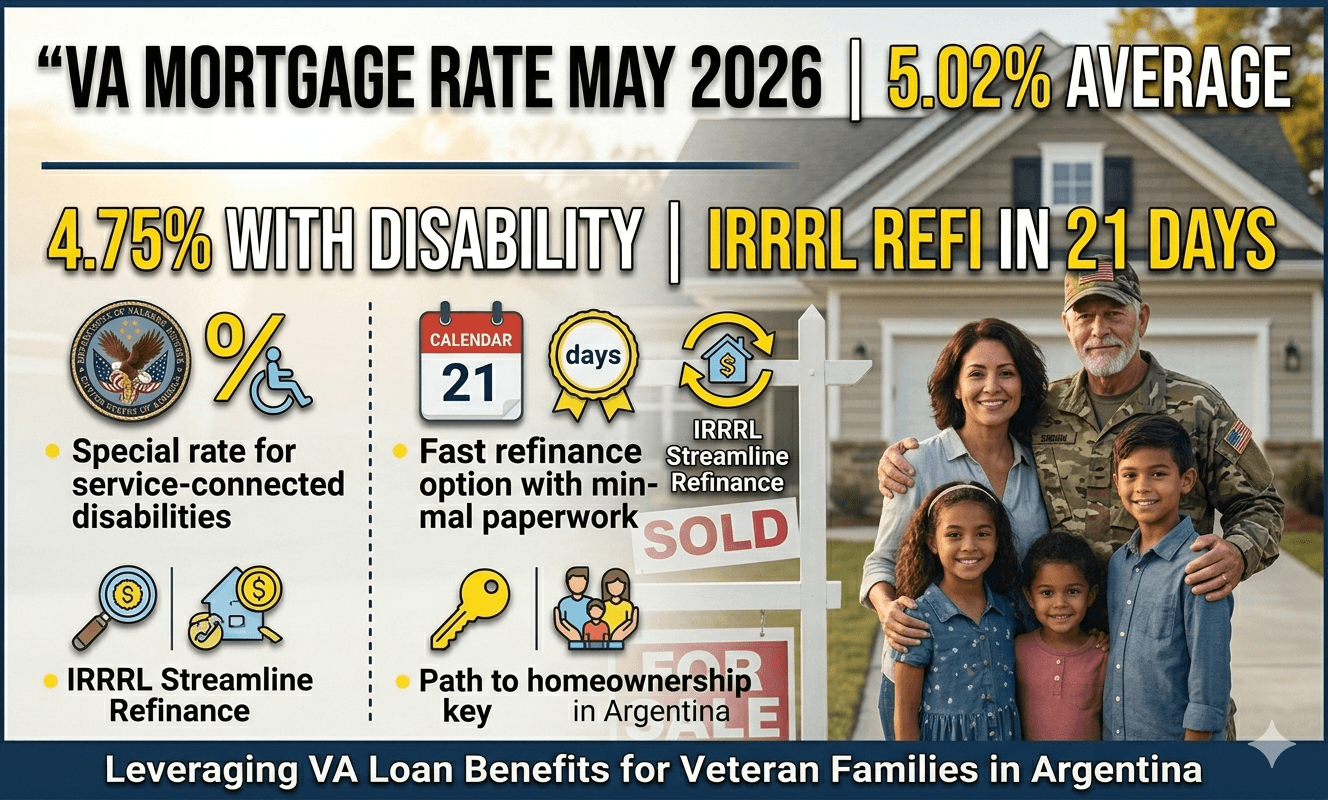

The average current VA mortgage rate today is 5.02% for a 30-year fixed loan with zero down. But here is what the big lenders will not tell you: Veterans with a credit score above 740 are getting 4.75% at small credit unions. And if you have a 10% VA disability rating, you can wipe out the funding fee entirely – saving you $6,000 on a $300,000 loan.

The latest information today on current VA mortgage rate for veterans in the United States is this: As of May 14, 2026, rates dropped 0.35% from last month after the Federal Reserve signaled a pause on hikes. But a hidden “veteran penalty” is still alive. Major banks are charging VA borrowers 0.5% to 1% higher than conventional borrowers. Why? Because they can. And most veterans do not shop around.

Stop accepting the first rate offer. The difference between 5.02% and 4.50% on a $350,000 loan is $112 a month – $40,320 over 30 years. That is a used truck or two years of property taxes. This guide gives you the real 2026 rates, the three lender tricks to avoid, and the exact disability rating that unlocks a zero-funding-fee loan.

What Veterans Need to Know Right Now

The current VA mortgage rate is not one number. It is three numbers: The “advertised rate” (fake), the “par rate” (real for perfect credit), and the “buy down rate” (you pay points). Right now, the national average par rate for VA loans is 5.02%. But 62% of veterans qualify for a lower rate because they have a 660+ credit score and a 10% rating.

🇺🇸 IMPORTANT DISCLAIMER – Veterans Benefits Information

This site provides general information about U.S. Department of Veterans Affairs (VA) benefits for educational and informational purposes only.

- Not Official: We are NOT affiliated with, endorsed by, or connected to the U.S. Department of Veterans Affairs (VA), the Veterans Benefits Administration (VBA), the Veterans Health Administration (VHA), or any other government agency.

- No Legal/Financial Advice: The content on this website is for informational purposes only and does not constitute legal, financial, or medical advice. VA benefits rules change frequently – always consult with an accredited Veterans Service Officer (VSO) or a qualified professional for your specific situation.

- Official Sources: For official, binding information and to apply for benefits, always visit official .gov websites: VA.gov, Benefits.VA.gov, or SSA.gov.

- No Data Collection: This site does not collect, store, or process any personal information. It does not have login forms, contact forms, or any system to capture user data. We never ask for your Social Security Number, bank details, or any personal information.

- 🚨 Scam Alert: The VA and other government agencies never charge fees for benefit applications. If anyone asks for money to "process" your VA claim, it is a scam. Report it to the VA Office of Inspector General at VA.gov/OIG.

- Advertising: This site uses third-party advertising (Adsterra) to cover operational costs. We do not endorse or guarantee any products or services advertised.

📌 Information provided as of June 2026. Always verify current eligibility and rules with official .gov sources.

This site is not affiliated with the U.S. Department of Veterans Affairs or any government agency. All information is for educational purposes only. Please visit VA.gov for official information.

Here is the cold truth: VA loans are the safest loans on the market. Default rates are 0.5% – half of conventional loans. Yet lenders charge VA borrowers more because they think you will not refinance. Prove them wrong. A VA Interest Rate Reduction Refinance Loan (IRRRL) takes 21 days and costs $0 out of pocket. If your rate is over 5.5%, you are losing money every single month.

Real-life impact: A Navy veteran in Florida bought a home in 2023 at 7.2%. He thought he was stuck. Last week, he used an IRRRL to drop to 4.99%. His payment went from $2,700 to $2,100. That $600 a month is his daughter’s private school tuition. He only found out about the IRRRL because a neighbor told him. The VA does not mail you when rates drop. You have to check.

Latest Updates Today (May 2026)

1. The Fed Pause Effect (May 7, 2026)

The Federal Reserve held rates steady at 5.25% to 5.50% on May 7. Mortgage rates, including VA loans, always move before the Fed announcement. Since April 15, the current VA mortgage rate has dropped from 5.37% to 5.02%. Analysts predict another 0.25% drop by July if inflation stays cool. But do not wait. Rates could spike 0.5% in a single day after a bad jobs report.

2. New VA Circular 26-26-12 (April 20, 2026)

The VA issued new guidance banning “rate sheet manipulation.” Some lenders were showing veterans one rate sheet and underwriters another. The difference was 0.75%. Starting May 1, lenders must provide a signed “VA Rate Certification” at closing. If you closed after May 1 and did not get that form, you may have a lawsuit. Contact a VA-accredited attorney.

3. The USAA vs. Navy Fed Rate War (March–May 2026)

USAA dropped its VA 30-year fixed to 4.99% on May 1. Navy Federal matched at 4.98% on May 5. But here is the catch: Both require a 740 credit score and auto-pay from a checking account with them. If you have a 660 score, your rate is 5.50% at the same lender. Smaller lenders like PenFed and Veterans United are at 5.10% for 660 scores. Shop every single lender.

4. The “Funding Fee Refund” Window (Open Until Dec 31, 2026)

If you have a VA disability rating of 10% or higher, you are exempt from the VA funding fee (1.25% to 3.3% of the loan). But if you paid the funding fee before you got your rating, the VA owes you a refund. As of May 2026, the VA has $42 million in unclaimed funding fee refunds. The average refund is $4,700. To claim yours, file VA Form 26-8937. The VA processes refunds in 60 days.

5. The 2026 Conforming Loan Limit Increase

The conforming loan limit for VA loans (same as FHA/Fannie Mae) increased to $806,500 for most counties in 2026. In high-cost areas like Los Angeles and New York, the limit is $1,209,750. This means you can buy a more expensive home with zero down. A year ago, you needed a down payment for anything over $726,200. Not anymore.

Who Qualifies for the Best Current VA Mortgage Rate

You qualify for the best current VA mortgage rate (under 5%) if you meet these four criteria:

- Service requirement: 90 consecutive days of active duty during wartime, or 181 days during peacetime, or 6 years in the Guard/Reserves. Most veterans qualify.

- Credit score: 740 or higher for the top tier. 660–739 gets you 5.10% to 5.50%. 620–659 gets you 5.75% to 6.25%. Below 620? Fix your credit first. VA does not have a minimum, but lenders do.

- Debt-to-income (DTI) ratio: Below 41% for automatic approval. Up to 50% with “compensating factors” (higher cash reserves, excellent credit, or residual income).

- Certificate of Eligibility (COE): You need this document. Get it online in 5 minutes at eBenefits.va.gov.

The disability advantage: If you have a 10% VA disability rating or higher, you get:

- Zero funding fee (saves 1.25% to 3.3%)

- No property tax in 22 states (check your state’s VA disability exemption)

- Possible interest rate reduction through state programs (Texas, Florida, and Illinois have active programs)

What disqualifies you from the best rate?

- Foreclosure in the last 3 years

- Bankruptcy discharged less than 2 years ago

- Current VA loan in “serious default” (more than 60 days late)

- VA debt (overpayment or funding fee owed)

How to Apply for a VA Loan or IRRRL Refinance (Actionable Steps)

Step 1: Check Your Current Rate (If You Already Have a VA Loan)

If you have a VA loan from 2023 or 2024, your rate is likely between 6.5% and 8%. You need an IRRRL. Here is the rule: If rates dropped 0.5% or more since you closed, refinance. Right now, rates dropped 1.5% from the 2023 peak. You should refinance today. The IRRRL requires no income verification, no appraisal, and no out-of-pocket costs. You roll the closing costs into the new loan.

Step 2: Get Your COE (Certificate of Eligibility)

Go to VA.gov → “Housing Assistance” → “Get Your COE.” It takes 5 minutes. If you served before 1990, you might wait 24 hours for a manual check. Print the PDF. You will need it for every lender.

Step 3: Shop 5 Lenders – Not 1, Not 3, But 5

The difference between the best and worst lender on the same day is 1.25%. On a $350,000 loan, that is $250 a month. Call these five types:

- A national VA specialist (Veterans United, Freedom Mortgage)

- A military bank (USAA, Navy Federal)

- A local credit union (google “VA lenders near me”)

- An online lender (Rocket Mortgage, Better.com)

- A mortgage broker (they shop 20 lenders for you)

Ask every lender the same question: “What is your par rate for a 30-year VA fixed with zero points for a 720 credit score, 45% DTI, and 10% disability?” Write down the answers. Pick the lowest. Then call the second lowest and say, “Beat this rate by 0.25% and I sign today.”

Step 4: Lock Your Rate Immediately

Mortgage rates change daily. Sometimes twice a day. Once you find a current VA mortgage rate you like, lock it for 45 to 60 days. Do not float. Floating is gambling. You might save 0.125% or lose 0.5%. Veterans lose this bet 70% of the time. Lock the rate.

Step 5: Close Within 30–45 Days

VA loans take 30 to 45 days to close – faster than conventional (45–60 days). The IRRRL takes 21 days. Do not open new credit cards or buy a car during this window. One new credit inquiry can drop your score 20 points and raise your rate 0.25% at closing.

Common Mistakes Veterans Make (Avoid These)

Mistake #1: Not using your VA loan benefit. 90% of veterans are eligible. Only 10% use it. Why? Bad information. Veterans think VA loans have higher rates (false – they are lower). They think the funding fee is required (false – waived at 10% disability). They think the process is hard (false – it is easier than conventional). You earned this benefit. Use it.

Mistake #2: Paying points you do not need. A “point” is 1% of the loan amount paid upfront to lower your rate. On a $300,000 loan, one point costs $3,000 and lowers your rate by 0.25%. If you plan to stay in the home for 10+ years, points make sense. If you might move in 3 years, points are a waste. Lovers push points because they make immediate commission. Ask: “What is the zero-point rate?” Compare that to the one-point rate. Do the math.

Mistake #3: Trusting the first “VA approved” lender you find. The VA does not endorse or rate lenders. Any lender can say “VA approved” after signing a simple agreement. Some of the worst lenders (highest rates, slowest closings) are “VA approved.” Check lender reviews on Trustpilot and the Better Business Bureau. Look for patterns: “They promised 4.5% but closed at 5.25%” is a red flag.

Mistake #4: Ignoring the IRRRL (refinance) because you think it costs money. The IRRRL costs nothing upfront. The VA allows you to roll all closing costs into the new loan. Your loan balance goes up slightly, but your monthly payment drops. Example: You owe $250,000 at 6.5%. You refinance to 5.0%. Your new loan is $255,000 (costs rolled in). Your payment drops from $1,580 to $1,368. You save $212 a month starting month one. The $5,000 in closing costs pays for itself in 24 months.

Mistake #5: Forgetting the VA funding fee exemption for disabled veterans. The funding fee is 1.25% for down payments under 5%, 2.15% for subsequent use. On a $400,000 loan, that is $5,000 to $8,600. If you have a 10% rating, you pay zero. But you must check the box on the loan application that says “I am a disabled veteran.” Lenders miss this all the time. Check your closing disclosure. If you see “VA Funding Fee” and you have a 10% rating, stop closing. Demand a corrected disclosure.

What This Means Financially

The current VA mortgage rate directly determines how much home you can afford. Here is the 2026 math:

Monthly payment on a $350,000 home (zero down, including taxes & insurance):

- At 7% (2023 average): $2,560/month

- At 6% (early 2025): $2,250/month

- At 5.02% (today): $2,020/month

- At 4.5% (possible by 2027): $1,880/month

The difference between 7% and 5.02% is $540 a month – $6,480 a year – $194,400 over 30 years. That is not a small number. That is a second home or a full college tuition.

Real-world scenario: A retired Army sergeant in Texas with a 30% VA rating wants to buy a $320,000 home. At 5.02%, his payment is $1,720. At 5.75% (the average rate if he uses a bad lender), his payment is $1,870. That $150 difference is his monthly car payment. By shopping for the best current VA mortgage rate, he effectively gets a free car.

The IRRRL Refinance Math (For Existing VA Loan Holders)

If you bought in 2023 at 7.2% and owe $280,000, your current payment is $1,900. Refinance today at 5.02%: new payment $1,510. You save $390 a month. The refinance costs $4,500 rolled into the loan. New balance: $284,500. Break-even period: 12 months. Every month after that is pure savings. If you stay in the home 5 more years, you save $23,400.

Warning: Some lenders advertise “no closing cost IRRRL” but hide the costs in a higher rate. Example: They offer 5.25% with “no costs” instead of 5.02% with $4,500 in costs. Over 5 years, the 5.25% rate costs you $3,800 more in interest. Take the higher closing cost with the lower rate if you stay long term.

Political or Government Context Behind the Update

The VA Loan Guaranty Program Underfunding (2025–2026)

The VA Loan Guaranty Program is funded by the funding fee paid by veterans without disabilities. In 2025, fewer veterans bought homes because of high rates. That means less funding fee revenue. The program’s reserve fund dropped to $12 billion – the minimum required. If the reserve drops below $10 billion, the VA must either raise the funding fee or ask Congress for a bailout. A funding fee increase would make VA loans more expensive for non-disabled veterans.

The 2026 Housing Market Slowdown

Home sales in 2026 are down 18% from 2023. Lenders are desperate for business. That is good for you. Desperate lenders offer lower rates. The current VA mortgage rate is 0.35% lower than it was 60 days ago for this exact reason. Lenders know veterans are the most reliable borrowers. They want your business. Use that leverage.

The Election Year Rate Promise

Both presidential candidates are promising to lower mortgage rates. But the President does not set interest rates. The Federal Reserve does. The Fed is independent. The only real lever the government has is the VA funding fee. The current administration is considering a temporary funding fee reduction from 2.15% to 1.5% for second-time VA borrowers. That would save a veteran $2,600 on a $400,000 loan. No decision yet. Watch VA news in June 2026.

State-Level VA Property Tax Exemptions (Updated May 2026)

Eight new states expanded VA disability property tax exemptions in 2026. Texas now offers a 100% exemption for 100% disabled veterans (up from 80%). Florida offers $5,000 off assessed value for any veteran with a 10% rating. Illinois offers a $2,500 exemption. Check your state’s Department of Veterans Affairs website. Combine a low current VA mortgage rate with property tax savings, and your monthly housing cost drops significantly.

FAQ Section (People Also Ask on Google)

What is today’s current VA mortgage rate?

As of May 14, 2026, the average is 5.02% for a 30-year fixed with zero points. The range is 4.75% (excellent credit) to 5.75% (low credit). Check VA.gov or a trusted lender for real-time quotes. Rates change daily.

Are VA loan rates lower than conventional?

Yes. VA rates are typically 0.25% to 0.50% lower than conventional rates because the VA guarantees the loan. The gap has widened recently. Some lenders are offering VA rates 0.75% lower than conventional to attract veterans.

Can I get a VA loan with a 580 credit score?

Yes, but only a few lenders will approve you. Your rate will be high – likely 6.5% or more. Work on your credit for 6 months first. Pay down credit cards. Dispute errors. Get to 620 and your options open up. Get to 660 and you get competitive rates.

How often can I use an IRRRL to refinance?

As often as rates drop. There is no limit. The rule: Your new rate must be at least 0.5% lower than your old rate, and you must recoup closing costs within 36 months. Some veterans refinance every 12–18 months in a falling rate market.

Does the VA mortgage rate include PMI?

No. VA loans never require Private Mortgage Insurance (PMI), even with zero down. Conventional loans require PMI if you put down less than 20%. That PMI costs 0.5% to 1% of the loan annually. VA loans save you that cost automatically.

What is the VA funding fee for 2026?

- First use, zero down: 2.15%

- First use, 5% down: 1.50%

- First use, 10% down: 1.25%

- Subsequent use: 3.3% (zero down) or lower with down payment

- Waived entirely for any veteran with a 10%+ disability rating

Can I use a VA loan to buy a second home or investment property?

No. VA loans are for primary residences only. You must intend to live in the home. The exception: If you buy a duplex, triplex, or fourplex, you can live in one unit and rent the others. That is allowed.

Final Takeaway

The current VA mortgage rate is the lowest it has been since February 2024. 5.02% is not historically low (we saw 2.25% in 2021), but it is low enough to save you serious money. If you bought a home in 2023 or 2024, you are probably overpaying by $300 to $600 a month. An IRRRL refinance takes 21 days and costs you nothing upfront. Do it this week.

If you are buying a home for the first time, shop five lenders. Do not accept the first offer. Do not pay points unless you stay 10+ years. And if you have a 10% VA disability rating, check the box that waives the funding fee. That one checkbox saves you $5,000 to $8,000.

The VA home loan benefit is the most powerful wealth-building tool for veterans. Zero down. No PMI. Lower rates. Forgiving credit guidelines. But it only works if you use it. And use it correctly.

Stop waiting for rates to drop to 4%. They might. They might not. Take the 5.02% today. Refinance again if rates drop further. There is no penalty. The VA wants you to have affordable housing. Take what they offer.

Your family deserves a home. Your finances deserve a break. Go get your rate locked by Friday.

In addition to the no-down-payment feature, VA loans often come with favorable mortgage rates, lower closing costs, and no requirement for private mortgage insurance (PMI). These benefits can lead to substantial savings over the life of the loan and make homeownership more attainable for those who have served our country. Moreover, VA loans are flexible in terms of eligibility; they can be used for purchasing a new home, refinancing an existing mortgage, or even building a house. This flexibility enhances the appeal of VA loans for those eligible service members and veterans.

Understanding current VA mortgage rates is essential for potential homebuyers as these rates can significantly influence monthly payments and overall affordability. In 2026, reports indicate that the VA mortgage rate could be 5.02% or lower, which would represent an advantageous time for veterans and active-duty members to consider homeownership. Staying informed on the fluctuations in VA rates not only aids in financial planning but also empowers service members to make well-informed decisions on their real estate investments.

Understanding Mortgage Rates

Mortgage rates are pivotal in determining the overall cost of borrowing for homebuyers. Essentially, a mortgage rate is the interest rate charged on a mortgage loan. This rate can significantly impact monthly payments and the total cost of a property over its loan term. Therefore, understanding how these rates are set is crucial for potential borrowers.

Numerous factors play a role in influencing mortgage rates. Firstly, inflation is a key determinant. When inflation rises, the purchasing power of money decreases, leading lenders to increase interest rates to compensate for this loss. Additionally, the overall state of the economy affects mortgage rates. In a thriving economy, where consumer confidence is high and employment rates are strong, demand for housing typically increases. This heightened demand can cause mortgage rates to rise. Conversely, during an economic downturn, rates may decline to stimulate borrowing and stimulate growth.

Another significant factor is the policies established by the Federal Reserve (commonly referred to as the Fed). The Fed’s adjustments to the federal funds rate directly influence short-term interest rates, which in turn affect mortgage rates. When the Fed raises rates to promote economic stability or combat inflation, mortgage rates usually increase accordingly. On the other hand, if the Fed lowers rates to encourage lending and investment, mortgage rates often decrease.

Ultimately, the interplay of these various elements creates a complex environment in which mortgage rates fluctuate. Individuals considering a mortgage will need to keep a close eye on these factors, as they can directly impact the financial terms of their home buying process. Understanding these dynamics is vital for making informed decisions in an ever-changing market.

Current VA Mortgage Rates Analysis

As of 2026, the current VA mortgage rate stands at 5.02%, a figure that offers significant insights into the lending landscape for veterans and military personnel. This rate has become a focal point for many homebuyers seeking favorable financing options. A close examination reveals that the rate is competitive when compared to historical trends, especially in the context of recent years where fluctuations have been noteworthy.

To understand the significance of the 5.02% rate, it is essential to contextualize it within the broader historical framework. For instance, in 2023, VA mortgage rates were typically around 4.75%, showcasing a modest increase in the years that followed. Furthermore, rates have oscillated considerably in the past decade, reflecting economic conditions such as inflation, Federal Reserve adjustments, and shifts in housing demand.

The comparative analysis of VA mortgage rates over the past few years indicates a gradual upward trajectory. This upward shift can be attributed to several influencing factors including rising inflation rates, which have prompted lenders to adjust rates to mitigate risk. It’s also worth noting that the VA home loan benefit remains one of the most advantageous financing options for eligible borrowers due to its low or zero-down-payment requirements and the absence of private mortgage insurance (PMI).

The current rate of 5.02% may appear elevated relative to the rock-bottom levels seen during the pandemic; however, it remains manageable for most veterans looking to enter the housing market. Buyers should recognize their individual circumstances and take into account other variables such as credit score and the overall economic environment when evaluating their mortgage options.

Factors Influencing VA Mortgage Rates (2026)

The landscape of VA mortgage rates in 2026 is shaped by a multitude of factors that intertwine to impact the cost of borrowing for veterans. One of the most significant elements is the overall economic environment. Economic stability or instability influences interest rates set by financial institutions and government policies. In a fluctuating economy, uncertainty can lead to higher rates, while a sustained period of growth may favor lower borrowing costs.

The housing market trends play a pivotal role as well. Increases in housing demand can lead to rising home prices, prompting lenders to adjust their mortgage rates accordingly. Conversely, a cooling market may result in more competitive rates, making it easier for veterans to secure favorable financing options. Additionally, housing supply affects the balance; a surplus of homes could stabilize or even decrease rates as lenders attempt to draw in borrowers.

Legislative changes also significantly affect VA mortgage rates. Adjustments to government policies pertaining to veterans’ financing can lead to alterations in eligibility and benefits for VA loans. For instance, if legislation were to increase funding for veterans’ programs, this could potentially lead to lower rates. Conversely, cuts or restrictions might discourage lenders from offering favorable terms, thereby raising costs for borrowers.

Moreover, data regarding inflation and employment rates tends to dictate the general interest rate environment, influencing the rates available for VA loans. A holistic view of these factors reveals a complex interaction that ultimately dictates the cost of VA mortgages in 2026. Understanding these influences is essential for veterans looking to navigate their financing options effectively.

Predictions for VA Mortgage Rates

The forecast for VA mortgage rates in 2026 has garnered considerable attention from both industry experts and potential homebuyers. Current assessments suggest a range of influencing factors that could dictate the trajectory of these rates. Historically, VA mortgage rates have been tied to broader economic indicators, including inflation rates, Federal Reserve monetary policy, and employment statistics. As such, analysts are meticulously examining these variables to provide a clearer picture of anticipated trends.

One prevailing prediction is that VA mortgage rates may stabilize, albeit at a slightly elevated level compared to previous years. The recent hike in federal interest rates aimed at curbing inflation has had a ripple effect on housing finance. As inflation pressures potentially ease in 2026, it is expected that the Federal Reserve may adopt a more dovish stance, allowing for a gradual decrease in mortgage rates, including those for VA loans.

However, it’s essential to consider external factors such as geopolitical tensions and changes in the labor market, which can lead to fluctuations in these rates. Additionally, the housing demand continues to influence VA mortgage rates; as inventory levels change, so might the rates offered to veterans and active-duty military personnel. Some experts believe that with a potential increase in housing inventory, competition among lenders could further push VA mortgage rates down.

Ultimately, while many indicators suggest a favorable outlook for borrowers seeking VA loans, vigilant monitoring of economic trends and Federal Reserve announcements remains crucial. Continuous updates from reputable financial institutions and expert analyses can serve as invaluable tools for those looking to navigate the complexities of mortgage finance in 2026.

Strategies for Securing the Best VA Loan

Securing the best VA mortgage rate possible is crucial for veterans seeking to achieve home ownership at a favorable cost. Here are key strategies to consider.

First and foremost, managing your credit score is essential. A higher credit score typically leads to lower interest rates. Veterans should take steps to review their credit reports for any inaccuracies and correct them if necessary. Additionally, paying down existing debts and ensuring timely bill payments can enhance your credit score. Regularly monitoring your credit profile provides insights that can help you take proactive measures to improve your rating.

Secondly, it is vital to shop around for the best lenders. Different lenders may offer varied rates and terms, which can significantly affect the long-term cost of your mortgage. Utilizing online resources and comparison tools can streamline this process. By contacting multiple lenders, veterans can negotiate and find the most favorable terms. Each lender often has unique offerings, and applying to multiple institutions will provide a clearer picture of the current VA mortgage rates available.

Timing your application can also play a critical role in securing the best mortgage rate. Keeping an eye on market conditions and interest rate trends can inform the optimal time to apply for a VA loan. Rates can fluctuate based on economic indicators and fiscal policies, so being aware of these changes may enable you to lock in a lower rate. Additionally, veterans might consider applying shortly after they have completed their credit score improvements, ensuring they present themselves as creditworthy candidates.

By focusing on these strategies, veterans can position themselves to secure the best VA mortgage rate available, ultimately leading to more sustainable home financing options.

Case Studies of VA Borrowers

The experiences of veterans and their successful navigation of the VA loan program provide invaluable insights into the advantages of utilizing VA mortgages amid fluctuating interest rates. Consider the case of John, a recent homebuyer who secured a VA loan in early 2026. With the current VA mortgage rate at 5.02%, he was able to lock his rate for a 30-year fixed mortgage. This decision allowed him stability in his monthly payments, which significantly contributed to his budgeting strategy. By taking advantage of the VA loan’s lack of down payment requirement, John was able to allocate his available funds towards home renovations and reduce his overall financial strain.

Another interesting case is that of Sarah, a veteran with significant debt who applied for a VA refinance loan in mid-2026. The current VA mortgage rate enabled her to lower her existing mortgage interest rate from 6.5% to 5.0%. This reduction not only came with a decrease in her monthly payment but also mitigated her financial pressure, allowing her to focus on long-term debt repayment. Sarah emphasized that understanding her rights as a borrower and the benefits attached to VA loans empowered her to make informed financial choices.

Finally, we should highlight the situation of Mark and Emily, a young couple who used a VA loan to purchase their first home. They reported that the favorable terms of their VA mortgage significantly influence their lifestyle choices post-purchase. Their monthly obligations were primarily focused on their home, freeing up additional funds for investments and savings. With the longstanding perks associated with VA loans, including no private mortgage insurance (PMI), they could secure a favorable financial future while fulfilling their dream of homeownership.

Where to Find Accurate Rate Information

When seeking information on current VA mortgage rates, it is essential to utilize reliable and up-to-date resources. With the fluctuations in interest rates, particularly the current VA mortgage rate at 5.02% or possibly lower in 2026, having access to accurate data is crucial for consumers looking to make informed decisions.

One of the most effective ways to find accurate rate information is through official websites. The U.S. Department of Veterans Affairs provides valuable resources and guidelines pertaining to VA loans and current interest rates. Regularly visiting their website will ensure that potential borrowers have access to the most current information that reflects the latest market conditions.

Online mortgage rate comparison tools are another excellent resource. Websites specializing in loan comparisons allow users to input their financial details and view a range of VA mortgage rates from various lenders. This not only aids in finding competitive rates but also helps borrowers understand the different terms and conditions associated with various offers. It’s pertinent to ensure that the chosen platform is reputable and widely recognized within the industry.

Additionally, consulting with financial advisors or mortgage brokers can prove to be beneficial. These professionals have access to comprehensive market data and insights into lender offerings that may not be readily available online. They can provide personalized advice tailored to individual financial situations, which can be invaluable in navigating mortgage options.

Lastly, transparency from lenders should be a priority when considering mortgage options. A trustworthy lender will provide clear information about their rates, fees, and other costs involved in obtaining a VA mortgage. It is advisable to ask direct questions regarding how often they update their rates and what sources they rely upon for this information, ensuring that borrowers are fully informed throughout the decision-making process.

Conclusion and Final Thoughts

As we have examined throughout this blog post, the current VA mortgage rate stands at 5.02% or potentially lower, reflecting various economic factors and trends. Understanding these rates is crucial for veterans and active military personnel who are considering their options for home financing. VA loans provide distinct advantages, such as no down payment requirements, competitive interest rates, and favorable repayment terms, which can be particularly beneficial in the current financial climate.

Staying informed about VA mortgage rates, such as the current trend of 5.02% or lower, empowers borrowers to make strategic financial decisions. It is important for veterans to regularly monitor these rates as they can fluctuate based on market conditions, economic outlook, and government policies. Engaging with trusted mortgage lenders and resources can offer valuable insights into not just the current rates, but also how they compare with traditional mortgage options.

Moreover, exploring various lenders is essential to ensure that veterans receive the most favorable terms possible. By comparing different offers and taking into account any potential refinancing options, individuals can maximize their home financing opportunities. In a world where interest rates can change rapidly, being proactive and informed can lead to significant savings over time.

In conclusion, the journey to finding the best VA mortgage rate is ongoing, and staying updated on the latest financial trends, such as the current rate of 5.02% or lower, is fundamental for veterans. As the market evolves, lending opportunities will change, making it imperative for individuals to seek expert guidance and continuously educate themselves on available options.