Veterans Group Life Insurance (VGLI) is a renewable term life insurance program tailored specifically for veterans who have served in the military. This crucial insurance offering allows eligible veterans to convert their Servicemembers’ Group Life Insurance (SGLI) coverage into VGLI after their military service ends. The transition to VGLI provides veterans with the opportunity to maintain life insurance protection during a critical period of adjustment following their separation from active duty.

The ability to convert SGLI into VGLI is significant for veterans and their families as it ensures continued financial security. After leaving the service, many veterans may face uncertainties including changes in employment status or family dynamics, making life insurance a necessary consideration. VGLI safeguards against financial burden by providing a death benefit that can alleviate potential hardships for the beneficiaries.

VGLI is not only accessible but also offers flexible terms, allowing veterans to apply for coverage in various amounts up to the maximum of their previous SGLI coverage, as long as they do so within one year and 120 days of discharge. Following this initial period, veterans may still apply for VGLI, but eligibility and coverage amounts may be subject to new conditions.

This program is especially essential as it reinforces the commitment to support veterans after their service by addressing their unique needs. VGLI stands as an important financial product that ensures veterans can maintain essential insurance coverage to protect their loved ones and secure their financial futures. With the number of veterans seeking coverage increasing, understanding VGLI and its benefits is paramount for those facing life after military service.

Coverage Options Available

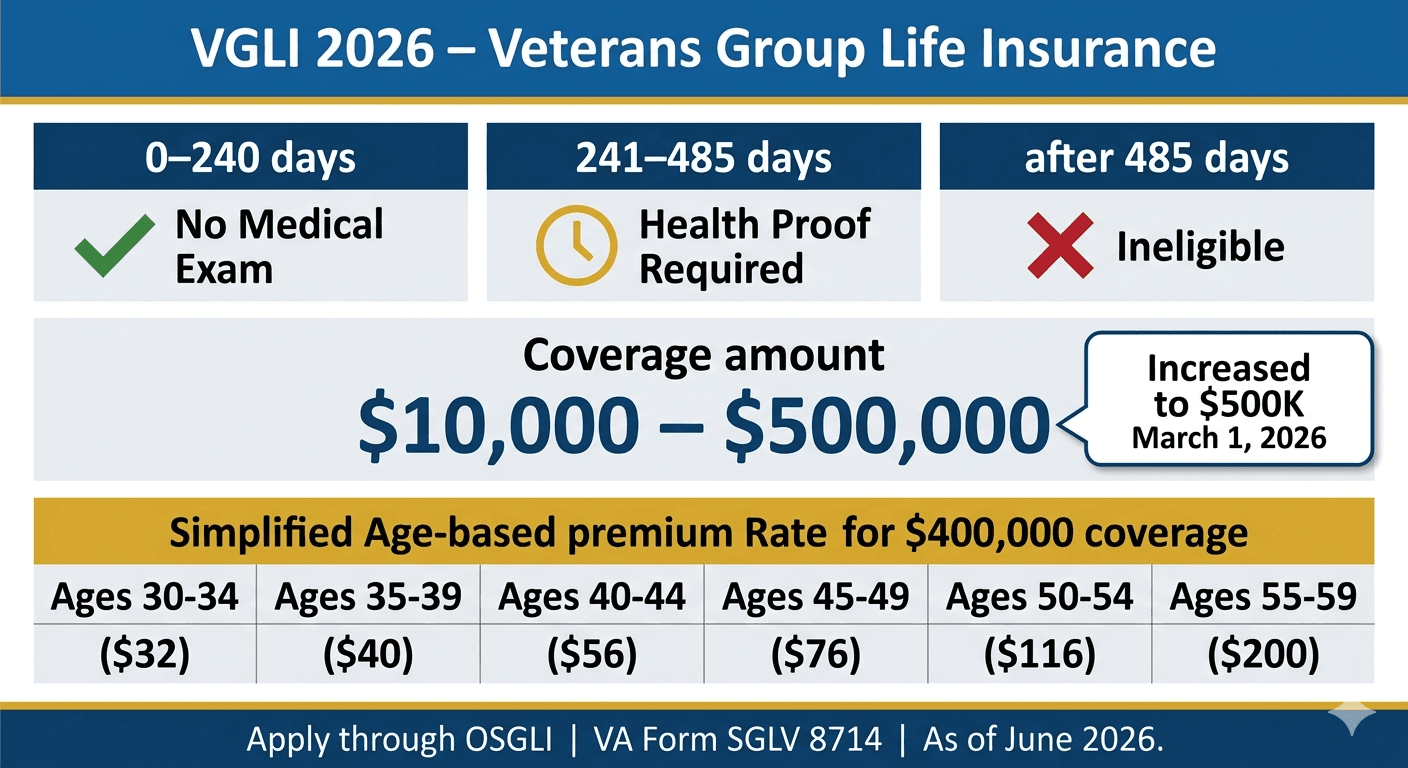

The Veterans Group Life Insurance (VGLI) program offers a range of coverage options designed to meet the diverse needs of veterans. Coverage amounts can be selected in increments of $10,000, starting from a minimum of $10,000 up to a maximum of $500,000. This flexibility allows policyholders to tailor their life insurance needs based on personal circumstances, financial responsibilities, and future goals.

As of March 1, 2026, an important update to the VGLI program is the increase in maximum coverage from $400,000 to $500,000. This change marks a significant enhancement in the available benefits for veterans, enabling them to secure a higher level of financial protection for their beneficiaries. The increase responds to the evolving economic landscape and recognizes the importance of ensuring adequate insurance coverage in crucial life stages.

Individuals may find different coverage levels appealing based on their unique situations. For instance, a veteran with dependents may opt for a higher amount of coverage to ensure that their family is financially secure in the event of their passing. Conversely, a veteran with fewer financial obligations may choose a lower coverage level to correspond with their specific needs and preferences.

Overall, understanding the various VGLI coverage options is crucial for veterans as they navigate their insurance choices. By carefully assessing their personal and financial circumstances, veterans can make informed decisions about the amount of coverage that best suits them. Such thoughtful consideration will not only provide peace of mind but will also ensure that loved ones are protected financially after the veteran’s death.

Application Timeline: Key Deadlines

The Veterans Group Life Insurance (VGLI) program offers veterans vital life insurance coverage that is accessible within specific timeframes following military discharge. Understanding the application timeline is crucial for veterans to ensure they receive this valuable benefit. After separation from military service, veterans have a one-year period during which they can apply for VGLI. This timeline begins on the date of discharge. Within this window, the application can be completed without demonstrating good health or undergoing a medical exam, ensuring easy access to coverage.

Furthermore, there is a distinct 120-day window that falls within the broader one-year period. This specific interval allows veterans to take advantage of guaranteed acceptance, provided they submit their applications within these 120 days after their discharge. During this timeframe, veterans can rest assured knowing that they will not be denied coverage based on health-related issues. This feature of the VGLI program is particularly beneficial for those who may have pre-existing medical conditions, enabling them to secure life insurance when it is most needed.

It is essential for veterans to meticulously track these deadlines to avoid any lapse in coverage. The 240-day period, starting from the discharge date, is a crucial point for application submission. As such, veterans are encouraged to consult the official VGLI guidelines or seek assistance from veterans’ organizations for information on the application process. By adhering to these key deadlines, veterans can ensure they do not miss out on the opportunity to secure financial protection for their loved ones through VGLI.

Guaranteed Acceptance: No Medical Exam Required

One of the defining features of Veterans Group Life Insurance (VGLI) is its provision for guaranteed acceptance of applications submitted within 240 days of a service member’s separation from active duty. This unique benefit sets VGLI apart from many conventional life insurance policies, which typically mandate a medical exam and comprehensive health disclosures before coverage is granted.

For veterans, the prospect of having guaranteed acceptance is significant, particularly considering the challenges they may face when securing life insurance. Traditional life insurance options often involve stringent underwriting processes, where applicants must undergo medical examinations and complete lengthy questionnaires detailing their medical histories. In contrast, the guaranteed acceptance offered by VGLI provides peace of mind, as veterans can quickly obtain insurance without the worry of being denied based on pre-existing health conditions.

This simplified approach to securing life insurance is especially crucial for veterans who may have encountered health issues stemming from their service. Since VGLI waives medical exam requirements during the application process, it is accessible to a broader range of applicants. The guarantee of acceptance enables veterans to obtain coverage swiftly and allows them to focus on their transition to civilian life rather than medical concerns related to insurance qualifications.

Moreover, VGLI allows veterans to retain coverage even as their health changes over time. This reassures those who, due to various circumstances, may find it difficult to qualify for other insurance options in the future. As such, veterans can rest assured knowing they have a viable insurance solution that remains in effect regardless of their medical status, further enhancing the attractiveness of VGLI as a primary life insurance option.

Transitioning from SGLI to VGLI

The transition from Servicemembers’ Group Life Insurance (SGLI) to Veterans Group Life Insurance (VGLI) is a crucial step for service members who have completed their military service. Understanding the conversion process is essential to ensure that veterans retain vital life insurance coverage post-service. This guide outlines the necessary steps for a smooth transition.

Initially, veterans should be aware that the transition must occur within one year and 120 days from the date of separation from active duty. It is beneficial to initiate this process as early as possible to avoid any gaps in coverage. Veterans should contact their SGLI office or utilize resources available through the Department of Veterans Affairs (VA) to begin the conversion.

To convert SGLI to VGLI, veterans need to complete the application process, which may include providing proof of good health. However, individuals who apply within the specified timeline are eligible to transition without undergoing a medical examination. This provision facilitates a smoother conversion and ensures veterans maintain their insurance benefits.

Once the application is submitted, veterans can expect to receive their VGLI policy within 60 days, assuming all documentation is in order. It is also important to note that the premium rates for VGLI may differ from SGLI rates and that these premiums can change based on the veteran’s age and coverage amount selected. Therefore, reviewing these rates carefully is necessary when deciding on the appropriate amount of coverage.

In addition to understanding the timeline and application process, veterans should familiarize themselves with the differences between SGLI and VGLI. While both policies serve the critical function of providing life insurance, VGLI allows veterans to maintain coverage without the need for reapplication in the future, as long as premiums are paid on time. This aspect significantly enhances the stability of the veteran’s financial planning, ensuring continued protection for themselves and their beneficiaries after military service.

Understanding Premiums and Rate Changes

Veterans Group Life Insurance (VGLI) offers an important form of coverage for veterans transitioning from active service to civilian life. Central to this insurance is the structure of premiums, which are categorized based on age bands. This age-banded system ensures that as individuals age, their premiums correspond to an increased risk associated with aging. Consequently, veterans may observe a natural increase in their premiums as they progress through different age bands.

Every five years, VGLI reassesses its premium rates, which can lead to adjustments that reflect broader actuarial data and financial considerations. Notably, recent rate adjustments that took effect on July 1, 2025, have been favorable, as they see reductions between 2% and 17%. This change is significant for many veterans, as lower premiums can lead to enhanced affordability of coverage, impacting their decisions regarding maintaining or expanding their insurance plans.

The implications of these adjustments extend beyond mere cost. For many veterans, the affordability of VGLI is a crucial factor that influences their ability to secure insurance in their later years. A reduced premium rate not only eases the financial burden but may also encourage veterans to choose VGLI over other potentially more expensive life insurance options available in the private market. This flexibility can ultimately affect a veteran’s long-term financial planning and security.

In light of the recent changes in premium rates, veterans are encouraged to reassess their policies and evaluate their insurance needs. Adjusting coverage levels to align with current premiums may lead to better-suited financial strategies for veterans, particularly as they navigate various stages of life. Understanding these age-based premium structures and the timing of rate changes is essential for veterans to make informed decisions regarding their insurance needs.

Life Insurance Needs Assessment for Veterans

Assessing life insurance needs is a crucial step for veterans seeking to secure financial stability for their loved ones after their passing. Veterans Group Life Insurance (VGLI) offers options that can cater to various personal and family circumstances. To begin evaluating life insurance needs, veterans should first consider their current financial obligations. These may include outstanding debts such as a mortgage, student loans, or credit card balances, which could burden surviving family members if left unpaid.

Next, consider the living expenses that would need to be covered. This includes day-to-day costs such as housing, utilities, and educational expenses for children. A thoughtful assessment of these factors will help in determining the appropriate coverage amount required through VGLI. One approach to calculating this is to use the “Income Replacement Method,” which estimates how many years of income would need to be replaced to maintain the family’s standard of living. Generally, a multiple of the veteran’s annual salary can serve as a reliable benchmark.

Additionally, veterans should take into account any existing life insurance policies, savings, or investment accounts that could supplement VGLI benefits. Assessing these assets will help prevent over-insurance. It is also vital for veterans to contemplate their family structure and specific needs. For example, dependents with special needs may require long-term financial support, thus necessitating a larger insurance policy.

When applying for VGLI, thorough preparation is key. Veterans should gather relevant financial information and reflect on their family’s future goals. Consulting with a financial advisor experienced in veterans’ benefits can further provide tailored insights and enhance decision-making efficacy. Ultimately, a well-rounded life insurance assessment can considerably benefit veterans and their families by ensuring they are adequately protected, no matter the circumstances.

Common Questions and Misconceptions about VGLI

Veterans Group Life Insurance (VGLI) is a vital resource for veterans seeking life insurance coverage tailored to their unique circumstances. However, there are several common questions and misconceptions surrounding this program that can lead to confusion among potential beneficiaries.

One prevalent misconception is that VGLI is not available to all veterans. In reality, eligibility is granted to veterans who had Servicemembers’ Group Life Insurance (SGLI) and choose to convert their coverage to VGLI upon separation from military service. This means that as long as you are within the eligibility window, you can secure coverage without undergoing a medical examination, making VGLI a convenient option.

Another area of confusion often pertains to the differences between VGLI and civilian life insurance policies. Unlike typical civilian life insurance, VGLI provides veterans with the security of continued coverage that is not subject to the same stringent health assessments that might affect civilian applications. VGLI coverage amounts can range from $10,000 to $400,000, allowing for flexibility according to individual needs, though the initial amount should align with the veteran’s previous SGLI coverage.

Many potential policyholders also wonder about the impacts of age and health on VGLI premiums. It’s important to note that premiums for VGLI are based on age, and they increase every five years once the veteran reaches certain age brackets. However, these premiums remain competitive compared to other options available to veterans. In contrast to civilian insurance, health issues do not impact eligibility or coverage, providing a safety net for those with pre-existing conditions.

The complexities surrounding VGLI can lead to many unanswered questions. Veterans are encouraged to reach out to the Department of Veterans Affairs or appointed counselors to clarify any doubts and enhance their understanding of how VGLI can fit into their broader financial and health plans.

Conclusion: Importance of Securing Insurance Coverage as a Veteran

As we have explored throughout this blog post, Veterans Group Life Insurance (VGLI) is a vital resource for veterans seeking life insurance coverage. Understanding the specifics of VGLI allows veterans to make informed decisions regarding their financial protection and the wellbeing of their loved ones. This program provides an opportunity to convert existing service-related life insurance into lifetime coverage, which is especially significant considering the unique challenges that veterans may face when transitioning to civilian life.

Securing life insurance coverage through VGLI not only offers financial security but also instills a sense of peace of mind for veterans and their families. The potential for unforeseen circumstances creates an undeniable need for reliable life insurance. A policy under VGLI can alleviate the burden of financial stress, providing a safety net that supports the veteran’s family in times of crisis.

Moreover, the process of applying for VGLI is designed to be straightforward and accommodating for veterans, devoid of extensive medical exams or stringent eligibility assessments. This accessible approach is tailored to honor the service and sacrifices made by veterans, making it an indispensable option for those looking for life insurance coverage.

In light of the various benefits associated with VGLI, veterans are strongly encouraged to take advantage of this program. It not only ensures that loved ones are cared for in the event of a tragedy but also reinforces the commitment to veterans’ welfare as they navigate post-service life. Understanding the importance of securing insurance coverage is essential, as it goes beyond mere financial planning; it represents a proactive step towards safeguarding families and preserving legacies.

Ultimately, the peace of mind that comes with securing life insurance under programs like VGLI is invaluable. Taking action now will ensure that veterans and their families are protected for years to come, providing a sense of security that is critical in today’s unpredictable world.

🇺🇸 IMPORTANT DISCLAIMER – Veterans Benefits Information

This site provides general information about U.S. Department of Veterans Affairs (VA) benefits for educational and informational purposes only.

- Not Official: We are NOT affiliated with, endorsed by, or connected to the U.S. Department of Veterans Affairs (VA), the Veterans Benefits Administration (VBA), the Veterans Health Administration (VHA), or any other government agency.

- No Legal/Financial Advice: The content on this website is for informational purposes only and does not constitute legal, financial, or medical advice. VA benefits rules change frequently – always consult with an accredited Veterans Service Officer (VSO) or a qualified professional for your specific situation.

- Official Sources: For official, binding information and to apply for benefits, always visit official .gov websites: VA.gov, Benefits.VA.gov, or SSA.gov.

- No Data Collection: This site does not collect, store, or process any personal information. It does not have login forms, contact forms, or any system to capture user data. We never ask for your Social Security Number, bank details, or any personal information.

- 🚨 Scam Alert: The VA and other government agencies never charge fees for benefit applications. If anyone asks for money to "process" your VA claim, it is a scam. Report it to the VA Office of Inspector General at VA.gov/OIG.

- Advertising: This site uses third-party advertising (Adsterra) to cover operational costs. We do not endorse or guarantee any products or services advertised.

📌 Information provided as of June 2026. Always verify current eligibility and rules with official .gov sources.

This site is not affiliated with the U.S. Department of Veterans Affairs or any government agency. All information is for educational purposes only. Please visit VA.gov for official information.